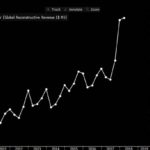

Alphabet reported very strong Q218 results, beating on sales and earnings. Google segment revenues were up 25% and other revenue, which includes cloud, was up 37%. Mobile search and YouTube continue to drive ad revenue. Importantly, traffic acquisition costs (TAC) were down as a percentage of revenue (23% of revenue vs 24% last quarter). This was a key positive in the quarter as TAC accounts for most of cost of sales. Management previously suggested this reversal was coming. Two dynamics have been driving higher TAC: the mix shift to mobile and to programmatic. Although these evolving ad formats monetize differently and are lower margin than desktop search they continue to represent meaningful growth opportunities. They report their ad revenues in two buckets: “Google Properties” (rev from search, Gmail, YouTube etc) and “Google Network Members” (rev from 3rd party sites that use AdSense, AdMob or DoubleClick to sell ads on their sites). Google Properties has lower TAC and is growing faster (>80% of ad revenue). Starting last quarter, they changed their monetization metrics. For Network Member properties they switched from reporting clicks (how many times people clicked on an ad) to impressions (how often ads are viewed). The change represents the growing importance of (higher TAC) programmatic on Network properties (which is largely monetized by impression). They also had solid performance in their non-ad businesses. Hardware is seeing strong growth and their cloud business continues to see momentum as they work to catch up with Amazon and Microsoft. Today (at their “Google Cloud Next” event) they announced an important new hybrid cloud solution that targets Microsoft Azure’s dominance in this space. This underscores the growing importance of hybrid solutions as cloud penetration increases. The CEO spent a lot of time on the call talking about applications of AI across their business and their opportunity in cloud. He echoed a similar sentiment that Satya Nadella (MSFT CEO) did last week – that despite AWS’s early lead, cloud should not be viewed as winner-take-all on a customer level because… “businesses are going to embrace multiple clouds over time.” He also indicated that he thinks cloud adoption is still in early stages and that “there’s a lot of opportunity.”

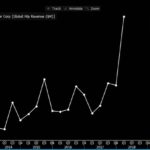

With the exception of lower TAC, this quarter follows a similar trend of rising expenses and investment impacting margins as they “invest ahead of growth.” Higher operating expenses are largely related to head count increases in R&D (tech talent) and sales & marketing. Capex continues to remain elevated, increasing from $2.8B in 2Q17 to $5.5B this quarter. This is a similar pace of growth as last quarter (ex the Chelsea Market purchase). They continue to invest in things like equipment and data centers. The investments in technical infrastructure reflect expanding applications of machine learning across the company.

[MORE]

Valuation:

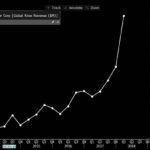

· FCF for the quarter was $4.7B and is expected to be $26B for the year.

· Trading at a ~3% FCF yield. Although the stock looks more expensive, it is on depressed FCF margins which should improve as capital intensity normalizes. No change in thesis.

· $98B in net cash, $140/share or 11% of their market cap.

Thesis on Alphabet:

· Online advertising as a share of overall Ad budgets will continue to grow as:

o People spend more time on the internet/mobile internet vs tv, radio, newspapers etc

o Higher ROI (+ easier to measure) per marketing dollar spent online vs other ad mediums

· They are the global leader in search.

· Well positioned to benefit from increased smartphone penetration.

· Flexible business model provides operating leverage with high returns ROIC and huge free cash flow generation.

$GOOGL.US

[tag GOOGL]

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

www.crestwoodadvisors.com

PLEASE NOTE!

We moved! Please note our new location above!