Current Price: $105 Price Target: $120

Position size: 5.5% TTM Performance: 11%

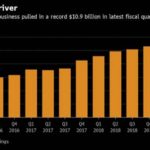

Microsoft reported a strong quarter with double-digit top and bottom line growth. Results were basically in-line with expectations – revenue was $32.5B (+13 YoY, constant currency) and EPS was $1.10 (+14% constant currency). Midpoint of top line guidance for Q3 slightly below the street. They say they continue to benefit from favorable secular trends and IT spending conditions. This was reassuring given some recent concern that IT spending is slowing. Results continue to be driven by their Commercial Cloud business which was up 48% reaching $9B. They saw flat gross margins overall and slight op margin improvement. Improving cloud margins were offset by a sales mix shift to commercial cloud and surface hardware. Free cash flow was $5.2 billion, down 2% YoY reflecting higher capex in support of their cloud business

Key Takeaways:

· Solid growth across all 3 segments:

o Productivity and business processes grew 13% (31% of revs) driven by LinkedIn revenue up 29% and Dynamics 365 up 51%. Office 365 Commercial revenue increased 33%, driven by seat growth of 27% and ARPU expansion from continued customer migration to higher-value offerings.

o Intelligent Cloud, which now includes GitHub, grew 20% (29% of revs). Azure is reported in this segment and grew 76%.

o More Personal Computing grew 7% (40% of revs).

§ Windows OEM revenue declined 5% due to weakness in consumer PCs that was negatively impacted from constrained chip supply.

§ Surface revenue grew 39%.

§ Gaming was up 8%. Gaming software and services are growing while hardware is declining.

§ They had their largest gaming revenue quarter ever with record avg. revenue per user. Xbox live now has 64 million active users.

§ They acquired another two studios this quarter, bringing the total to 13, more than doubling their first party content capacity in the past 6 months. The ambition is to build a world-class gaming platform spanning mobile, PC, and console. Like a Netflix of gaming.

· Commercial Cloud revenue (consisting of Office 365 Commercial, Azure, Dynamics Online, and LinkedIn Commercial, so pulls from the first 2 segments) was $9B, +48% YoY.

o Commercial cloud gross margin increased by 5 pts YoY to 62% driven by significant improvements in Azure gross margin.

o Within Commercial Cloud, Azure grew 76%. This suggests annual revenue for Azure close to $13B.

· Nadella again talked about their competitive advantage as a vendor enterprises can trust, whereas AMZN is often a competitor with companies it seeks as clients for their cloud business.

· Management expects a 100-200bps headwind from FX in 3Q19.

Valuation:

· FCF in the quarter was $5.2B. Returned $9.6B to shareholders ($3.5B in dividends and $6.1B in share repurchases).

· Trading at a 4.4% FCF yield – reasonable for a company with double digit top line growth, high ROIC and a high and improving FCF margins.

· They easily cover their 1.8% dividend, which they have been consistently growing.

· Strong balance sheet with about $128B in gross cash, and about $60B in net cash.

· Price target based on ~30% FCF margins and mid-to-high single digit top line growth.

Investment Thesis:

· Industry Leader: Global monopoly in software that has a fast growing and underappreciated cloud business.

· Product cycle tailwinds: Windows 10 and transition to Cloud (subscription revenues).

· Huge improvements in operational efficiency in recent quarters providing a significant boost to margins which should continue to amplify bottom line growth.

· Return of Capital: High FCF generation and returning significant capital to shareholders via dividends and share repurchases.

$MSFT.US

[tag MSFT]

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

www.crestwoodadvisors.com