So far, 89% of the companies in the S&P 500 have reported results for Q4.

· Companies are reporting fewer than average beats (69%) and 2019 revenue and EPS growth estimates are coming down. The biggest beats are in the energy sector.

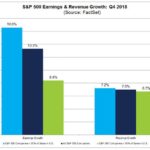

· Q4 revenue growth is 6.6% and EPS growth is 13%. That puts FY18 revenue growth at 8.8% and EPS growth at 20%.

· More companies are issuing negative EPS guidance for Q1 than average. Not all companies issue guidance, but of the 93 in the S&P that have so far, 73% issued negative guidance.

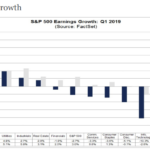

· For Q1, EPS growth is expected to be negative due to margin contraction. Revenue growth is expected to be up 5.2% and EPS growth down -2.7%.

· Growth is expected to decelerate for FY2019 to 4.9% revenue growth and 4.5% earnings growth. So margin contraction for the full year as well, but to lesser degree than Q1.

· Currency headwinds are a factor in the eroding growth that we’re seeing. Companies with higher global revenue exposure are reporting lower growth. The aggregate S&P geographic revenue exposure is 62% US and 38% international.

· The forward 12-month P/E ratio is 16.2.

· The Consumer Discretionary sector has the highest forward P/E ratio at 20.1x, while Financials has the lowest at 11.6x.

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109