On 7/21, Schwab hosted their summer update for Q2 earnings of $.48. Schwab reported solid core new asset growth of 5% as AUM reach $4.1t. Low interest rates remain a headwind with Net Interest Margin (NIM) falling to 1.53%. Rising deposits have helped offset falling NIM. Valuation remains attractive.

Despite lower interest rates, we remain optimistic that SCHW will continue to grow AUM significantly this year, leveraging its platform to drive ESP growth.

Current Price: $ 34.98 Price Target: $38 (down from $43)

Position Size: 1.6% Performance since initiation on 6/24/19: -9.0%

Q2 Highlights:

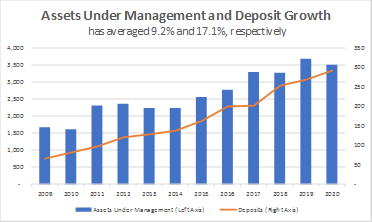

· Total client assets rose to $4.1T, with core new asset growth of 5%.

o Client assets are up 11% YoY

o Brokerage accounts up 18% YoY

o Core asset growth should remain healthy into 2020 with TD Ameritrade acquisition ($1.2t in AUM) which is expected to close second half of this year. Combined with core new growth of ~6% shows the potential growth in earnings power for SCHW as they lever their platform.

- Deposit growth of $24b up 8.6%

- Schwab continues to increase deposits at a pace faster than AUM growth as market volatility causes clients to raise cash.

- Investing $24b should increase revenue by $360, which represents a 15% increase in revenue, so these interest earning assets are significant.

- Schwab continues to increase deposits at a pace faster than AUM growth as market volatility causes clients to raise cash.

- Net interest margin

- Net Interest Margin (NIM) was 1.53% falling sharply from 2.14% in Q1, more than offsetting the growth in deposits as interest revenue fell 14%.

- NIM bottomed in 2013 at low 1.50%, and SCHW indicated that the floor this time might be 1.40%, so NIM will fall a bit from here. Hopefully we have already seen the sharpest declines and interest income starts to stabilize.

- Net Interest Margin (NIM) was 1.53% falling sharply from 2.14% in Q1, more than offsetting the growth in deposits as interest revenue fell 14%.

- Advice and Funds

- Schwab fee based advice solutions assets grew $263b up 2% YoY.

- Schwab revenue from funds and ETFs rose $452m up 2%

- Trading revenue fell 7%, but trading revenue has fallen to only 7% of income

- Schwab fee based advice solutions assets grew $263b up 2% YoY.

- Profitability – industry leader

- ROE 12% and 40% pre-tax profit margin

- Expenses up only 8%, of which 6% are due to mergers

- ROE 12% and 40% pre-tax profit margin

- Capital allocation

- Schwab will look to issue a preferred stock issue as growth in balance sheet and acquisitions will require more capital. Share buybacks are on hold.

- Dividend yield of 2.07%

- Valuation is attractive at 17x earnings. Target price set at 20x.

- Schwab will look to issue a preferred stock issue as growth in balance sheet and acquisitions will require more capital. Share buybacks are on hold.

Schwab Thesis:

· Expect Schwab’s vertically integrated business model to drive AUM growth. Schwab has averaged 6% organic core net new asset growth as retail clients and advisors are attracted to Schwab’s low cost trading and custody services.

· Conservative, well-managed firm who is a leader in online trading and focused on leveraging platform.

· Schwab will experience material AUM growth with USAA and TD Ameritrade mergers. Expect SCHW to reduce costs and leverage platform.

Please let me know if you have any questions.

Thanks,

John

$SCHW.US

[category earnings ]

[tag SCHW]

John R. Ingram CFA

Chief Investment Officer

Partner

Direct: 617.226.0021

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109