HILIX Commentary – Q4 2020

Thesis

Serving as a satellite holding, HILIX is a value style fund that takes advantage names that have underperformed recently and are cheaply priced. The team generates alpha by finding companies with strong fundamentals that are overlooked during times of low consensus expectations. We like that HILIX takes advantage of extremes and gains exposure to less efficient market caps by having more holdings and moderate active bets.

[more]

Overview

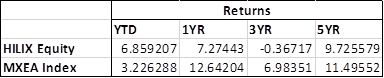

In the fourth quarter of 2020, HILIX outperformed the benchmark (MSCI EFEA Index) by 485bps due mainly to the fund’s allocation to Energy and Financials. An underweight to Health Care and Consumer Staples also contributed to return, as did strong stock selection within Industrials, Consumer Staples, and Information Technology. Selection in Developed Europe & Middle East ex UK also benefitted overall performance. Yet, exposure to Information Technology, selection within Materials, Communication Services, and Developed Asia Pacific ex Japan detracted from returns.

Q4 2020 Summary

- HILIX returned 20.90%, while the MSCI EAFE Index returned 16.05%

- Top issuer contributors

- Dongfeng Motor Group

- Bank of Ireland

- Top issuer detractors

- Barrick Gold

- Not owning Banco Santander

Outlook

- We continue to hold this fund and believe in our thesis due to the fund’s value and bottom-up, fundamental approach

- The fund saw heavy underperformance during most of 2020, but has since began to rally back in Q4 2020 and Q1 2021 as the “value” style continues to rebound

- The fund continues to focus on companies that are not trading at extreme valuations

- New positions include Japan Airlines and BAE Systems – both have strong balance sheets and low valuations

- Trimmed positions include Maersk and JSR – both trading at highs well above their fundamentals

- Value has been underperforming for some time, yet historically it has proven to outperform through full market cycles

[Category Mutual Fund Commentary]

Micah Weinstein

Research Analyst

Direct: 617.226.0032

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109