TCPNX Commentary – Q4 2020

Thesis

TCPNX is a smaller fund that does not have as many assets under management compared to our other core mangers, enabling them to make more nimble and tactical decisions. By making small allocations to undervalued “riskier” asset classes (high-yield and non-dollar denominated debt), TCPNX diversifies our fixed income portfolio and generates superior returns to the benchmark (Barclays U.S. AGG). We like that the fund utilizes a bottom-up investment process through proprietary framework analysis, fundamental security review, and portfolio risk management.

[more]

Overview

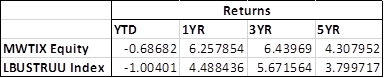

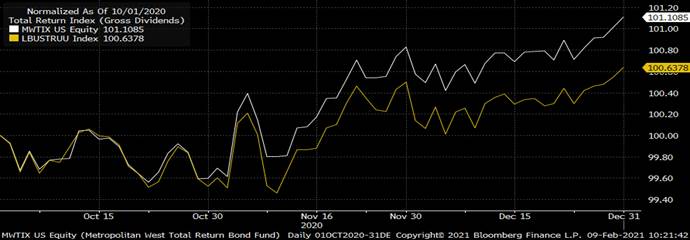

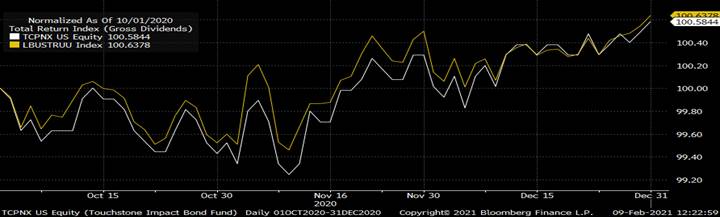

In the fourth quarter of 2020, TCPNX underperformed the benchmark (Barclays U.S. AGG) by 9bps primarily due to the headwind caused by the movement in credit spreads, which the fund has minimal exposure to. Allocations to U.S. Agencies and Agency Multi-Family MBS benefitted the fund, though. Additionally, all spread sectors nearly outperformed the equivalent U.S. Treasuries for the quarter. Yet lack of exposure to Industrials and Financials hurt performance, and the fund’s overweight to Utilities lagged compared to the other sectors.

Q4 2020 Summary

- TCPNX returned 0.58%, while the U.S. AGG returned 0.67%

- Quarter-end effective duration for TCPNX was 5.80 and 6.22 for the U.S. AGG

- Three largest contributors

- Airline Enhanced Equipment Trust Certificates, High Yield bonds, holdings in Kansas City Southern

- The top detractors

- Allocation to Utilities, U.S. Small Business Administration Development Company Participation Certificates, U.S. Treasury Separate Trading of Registered Interest and Principal of Securities

Optimistic Outlook

- We continue to hold this fund and believe in our thesis due to the fund’s consistent and defensive approach that we expect to generate alpha through times of low volatility

- Agreeing with the Fed in that there is not a big concern for a acceleration in inflation

- Continue to maintain a duration neutral portfolio, with a focus on spread products, SBA, and Agency Multi-Family MBS debt as they are positioned to benefit going forward

[Category Mutual Fund Commentary]

Micah Weinstein

Research Analyst

Direct: 617.226.0032

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109