Current price: $234 Target price: $260

Position size: 3.7% TTM Performance: 30%

Key takeaways:

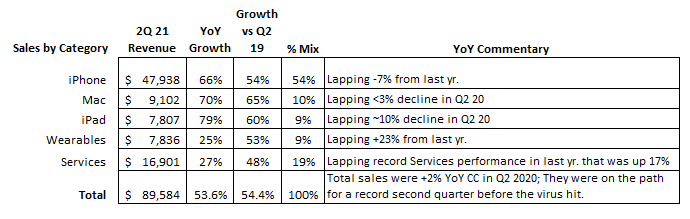

- Beat estimates – earnings and revenue beat

- Cross-border still a headwind but improving –driven by travel restrictions but Europe opening travel this summer w/ vaccines should be key to improvement.

- Payment volumes continue to improve and their net revenue and profits are at 2019 levels even as a rebound in travel (especially cross-border travel), still remains ahead of them.

- No guidance

- CEO Al Kelly said, “we believe we are starting to see the beginning of the end and the recovery is well underway in a number of key markets around the world… Cross-border travel is the slowest sector to return, but there are some green shoots that offer real indication of people looking to see the world.”

Additional Highlights:

- Revenues were down 2% YoY driven by cross-border headwinds (down 11% YoY or -21% YoY excluding intra-Europe), but mostly offset by growth in payments volume and processed transactions. Payments volume for the quarter increased 11% fueled by continued strength in debit as well as improving credit spending.

- Quotes from the call…

- “The pandemic has accelerated the digitization of cash, and we see the impact in debit and tap-to-pay. When we look at cash usage in the last 12 months just on the Visa brand, such as with ATM withdrawals, we see that global debit cash volumes have decreased by 7%, while debit payment growth has grown – payments volume has grown 16%, both on a constant dollar basis. This 20-point gap is more than double the historic gap in growth rates and relatively consistent globally, demonstrating cash digitization in both mature and emerging regions.”

- “There is significant pent-up demand for travel, in particular personal travel” and “The decline in travel is temporary, and we’re starting to see some early signs of recovery.” The vast majority of the travel Visa captures on their credentials is consumer, and they are the global leader in travel co-branded cards.

- Tailwinds building – pending travel recovery, re-opening beneficiary, accelerated cash digitization and growing e-commerce penetration…

- The most notable sign of a domestic recovery was card-present spend growing 4% which is up 3% over 2019, an 8 point acceleration from Q1 led by retail and restaurant spending.

- Credit has improved without debit slowing, pointing to accelerated cash displacement. The credit improvement was helped by increases in retail, travel, restaurant and entertainment spending mostly starting in early March as restrictions were relaxed in many states.

- Spend categories trends are starting to shift – for categories that were hardest hit by this pandemic including travel, entertainment, fuel and restaurants, spending remains depressed but is improving with re-opening.

- Cross border spending drives International transaction revenues which are >25% of total net revenues. As such, the steep drop is offsetting growth in service revs and data processing revs. As travel restrictions lift with the vaccine rollout, Visa will see a recovery in this meaningful piece of revenue. While cross-border spending did improve for the quarter (3 points better than Q1), it remains depressed (75% of 2019 levels), led by travel spending (down 55% YoY, still at 39% of 2019 levels), as the majority of borders remain closed.

- Crypto opportunity:

- “leaning into in a very, very big way, and I think we are extremely well positioned”

- Enabling purchases, enabling conversion of a digital currency to a fiat on a Visa credential, helping financial institutions and fintechs have a crypto option for their customers and upgraded their infrastructure to support digital currency settlement

- They have over 35 digital currency platforms/wallets that are working with them

- Working with Central Banks as digital currency is being explored in many nations

- Growth in “buy now, pay later”…

- Nascent but growing

- Visa is working with third party providers as well as offering their own proprietary platform that would allow issuers to offer their own buy now, pay later capability

- Potential for value-added services, data analytics to augment a provider’s underwriting or risk products to help some of the third-party providers.

- “we’re doing a lot in this space. We’re committed to it… I can’t predict exactly where it’s going to land, but we are going, to the degree it takes off, we’re going to be there to be part of it.”

- Growth areas…

- Consumer payments – digitizing the $18 trillion spent in cash and check globally. Continuing to grow acceptance (including contactless penetration) and grow credentials with traditional issuers, fintechs and wallets. In the last two years, they’ve grown their credentials to 3.6B and physical merchant locations to over 70m, up 7% and 34%, respectively. Notably, “merchant locations” only count partners like PayPal and Square each as one. LT opportunity to grow the pie for digital payments w/ the 1.7 billion unbanked.

- New Flows – $185 trillion in B2B, P2P, B2C and G2C. P2P, which represents $20 trillion of the opp., was Visa Direct’s first use case and continues to grow substantially. Visa Direct transactions grew almost 60% in 2Q. A key area of future growth is cross-border P2P, or remittance. Four of the top five global money transfer operators were onboarded in fiscal year 2020, TransferWise, Western Union, Remitly, and MoneyGram. In G2C, for example, Visa Direct supported the US government’s disbursements of economic impact payments to nearly 13 million Visa prepaid credentials so far this year.

- Value-added services – includes consulting, technology platforms (e.g. Cybersource, issuer processing, and risk identity and authentication), data and insights, and card benefits, all which will improve with the recovery. Opportunity to increase penetration w/ existing clients. In fiscal year 2020, more than 60% of their clients used at least five value-added services from Visa and more than 30%used 10 or more.

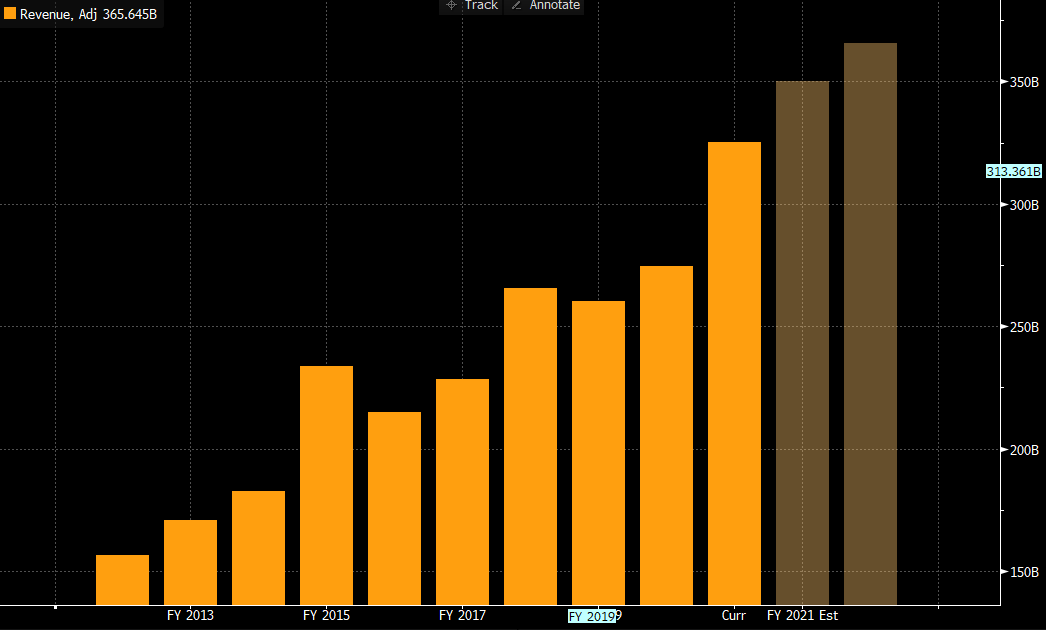

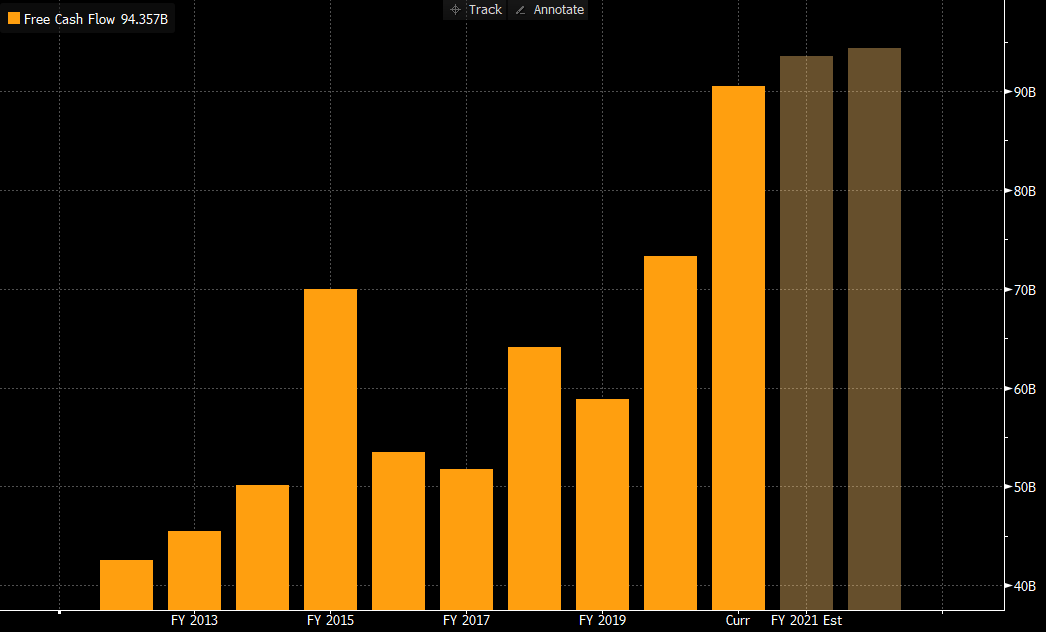

- While COVID has been a headwind for Visa, particularly in cross border volumes – the long-term thesis is intact. Visa is a high moat, duopoly company with extremely high FCF margins (approaching 50%), strong balance sheet and continued runway for secular growth driven by the shift from cash to card/digital payments and new payment flow opportunities. Getting more expensive, trading at <3% FCF yield.

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

$V.US

[category earnings]

[tag V]