Current Price: $325 Price Target: $355 (increased from $310)

Position size: 4.6% Performance since inception: +47%

Key Takeaways:

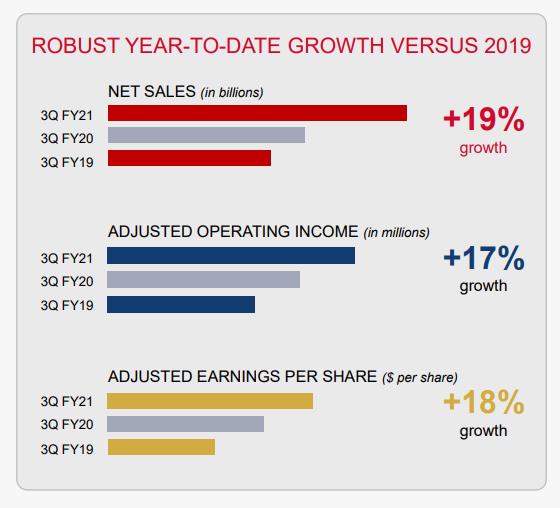

- Strong results and guidance. Revenue (+21%) in line w/ high end of guidance range. Upped full year revenue growth guidance to +12-15% YoY (7-10% organic) from previous guidance of +10% to +11%.

- Broad based strength in demand – They saw double-digit growth across all markets, all industry groups and all services. Consulting revenues for the quarter were $7.3B, up 29% and Outsourcing revenues were $6.1B, up 19%.

- Increased dividend 10% and increased buyback authorization

- Quotes from the call…

- “Technology is the single biggest driver of change in companies today and the depth, breadth and scale of our technology capabilities across our services is unmatched. We see the demand environment shaping up for FY ’22 to be more of the same… The vast majority of companies are early in their transformation and whether digital leader, leapfrogger, laggard or in between, all face multi-year journeys ahead of them because the re-platforming in the cloud and use of new technologies across the enterprise is a once in a digital era profound transformation.”

- “There remain entire parts of the enterprise for which digitization and the move to the cloud has only just begun. In particular, both the things companies make and the way they make things are being dramatically changed by technology and that is the focus of our Industry X business, which we believe is the next big digital frontier. In fact, a 2021 Gartner Survey of Board of Directors indicates that 93% expect that the number one business priority that we’ll see transformational improvement from digital technology is manufacturing, distribution and supply chain.” Their “Industry X” business is now ~$5 billion in revenue growing 36%.

- “sustainability is a critical area for which technology is still evolving. We believe that every business must be a sustainable business and yet companies are at very early stages of figuring out how to make this shift. Last year, building on years of investment and experience, we’ve launched our sustainability services under our new Chief Responsibility Officer and Global Sustainability Services Lead. We have continued to accelerate our focus in this expanding and changing market and are proud of the work we are doing with leading partners like Mastercard as we enhance its ability to track and analyze the carbon emissions of their suppliers and help decarbonize the UK Energy system with clients such as National Grid.”

- “With McCormick, a global leader in flavor in the food industry where we are partnering on a strategic transformation program encompassing finance, supply chain, logistics and plant maintenance. The new cloud-based platform and innovative data-driven approach will help standardize processes, increase efficiencies and support their goal of doubling in size quickly.”

- Bookings growth demonstrating momentum in the business – 20% increase in bookings to $59 billion. Overall book-to-bill of 1.1. Consulting book-to-bill of 1.1 and outsourcing book-to-bill of 1.2.

- Continued margin expansion – saw 30bps op margin expansion for the Q and 40bps for the full yr. despite higher attrition and significantly reinvesting in the business. They expect another 10 to 30bps expansion in FY22.

- Elevated utilization and attrition metrics driven by strong demand trends – Utilization remains elevated (~92%) as they try to keep up w/ demand. Attrition went up from 17% to 19%. This is slightly ahead of pre-pandemic levels and seems driven by incredibly high demand for talent in the current environment (as opposed to cultural issues w/ attracting/retaining talent) which could negatively impact profitability. Related to this, their record level “billable headcount” additions (~54K) this quarter is re-assuring.

- Demand outlook remains strong & Accenture is well positioned and taking share – Digital transformation is long-term secular growth driver to their business. “We are rapidly moving to a complete re-platforming of global business… it is hugely significant.” Accenture has an advantage w/ their unique positioning of trusted partner w/ leading edge technology expertise (they have >8K patents and their own network of R&D labs) combined with strategy and consulting practitioners that bring deep industry expertise. No competitor has their scale, breadth of services and cross-industry insights, which gives them an advantage in serving “compressed transformations.” “Our clients know that through our investments and focus on innovation, we will help future-proof them.”

- Accenture shines from an ESG perspective. They are a real leader in addressing how they create value for all of their stakeholders (employees, customers, vendors, shareholders) – it’s a constant theme on their calls, particularly w/ respect to their employees which is important as the “social” factor for them is very material b/c their industry is a “people business” w/ >600K employees across the globe. For instance:

- They’ve been heavily investing in upskilling their employees – they spent ~$900m in training this yr.

- Their workforce is now ~46% women; on track for their 2025 goal of a 50-50 gender balance.

- They have a top 3 ranking in the Refinitiv Global Diversity and Inclusion Index for the 4th consecutive year.

- They now have 50% renewable energy now powering their offices globally.

- They recently started their “360 degree value initiative” – aimed at helping their clients achieve responsible business goals – they say their clients are increasingly focused on sustainability, inclusion and diversity (rise of ESG is a catalyst to this) and that they are in a unique position to help companies w/ this.

- Capital allocation: exceeded original guidance for capital allocation by returning ~$6B of cash to shareholders while also investing >$4B (up from $2B) in acquisitions and >$1 billion in R&D. For FY22 they expect FCF of $7.5B to $8B and to return at least $6.3B through dividends and share repurchases.

- Valuation:

- The stock is undervalued trading at close to a 4% forward yield and they have an easily covered 1.2% dividend and no net debt.

- Multiple underpinned by ACN being a best-in-class company with stable growth that’s buffered by geographic and end market diversity and long-standing client relationships (95 of their top 100 clients have been with them for >10 years).

- They have $8B in cash on their balance sheet. The only debt they have on their balance sheet are capitalized leases, which were added last fiscal year due to an accounting change. Substantially all of their lease obligations are for office real estate.

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

www.crestwoodadvisors.com

$ACN.US

[tag ACN]

[category equity research]