DoubleLine Total Return Bond Fund Commentary – Q3 2021

Thesis

DBLTX (currently yielding 3.19%) utilizes a top down-bottom up process that focuses on MBS and Agency bonds. When compared to the benchmark (Barclays U.S. AGG), the holdings have lower duration and exposure to corporate bonds, reducing their sensitivity to interest rate movements and credit spreads. We expect attractive risk-adjusted return characteristics over the long term from DBLTX, especially during periods when corporate bonds’ spread increase and the yield curve steepens.

[more]

Overview

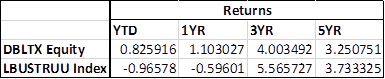

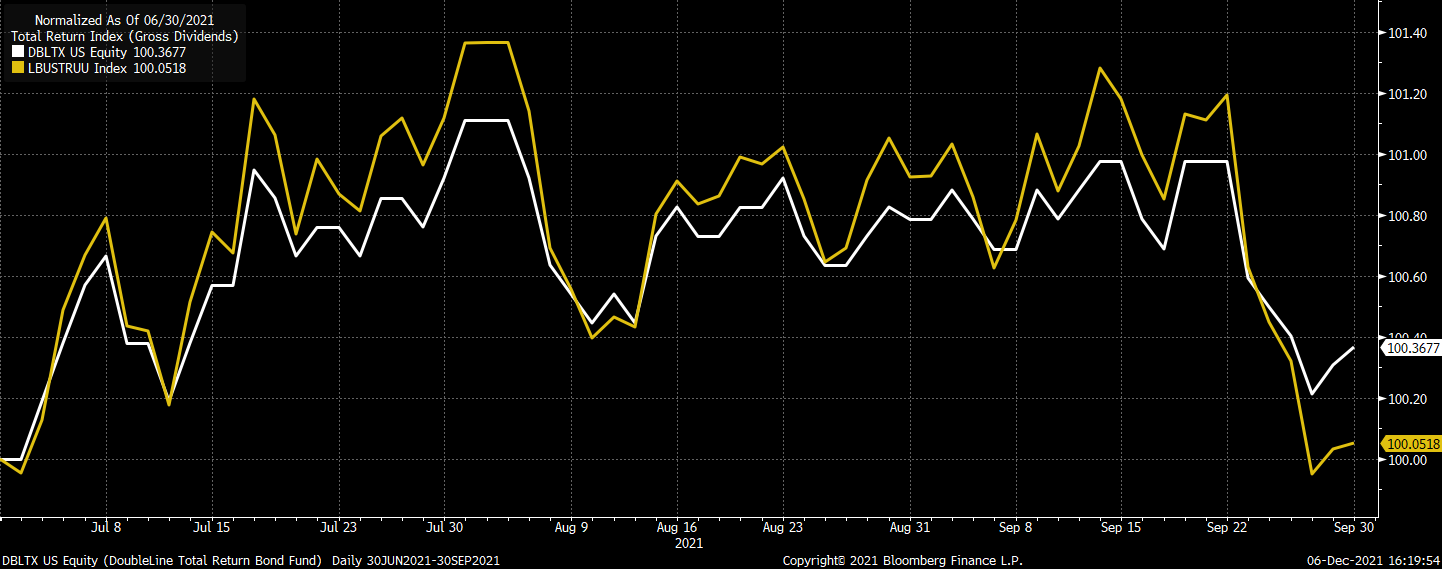

In the third quarter of 2021, DBLTX outperformed the benchmark (Barclays U.S. AGG) by 32bps, largely due to an overweight to credit. Exposure to non-Agency residential MBS and non-Agency CMBS also contributed to returns for the quarter. In general, every sector in the Fund acted as a tailwind to performance.

Q3 2021 Summary

- DBLTX returned 0.37%, while the U.S. AGG returned 0.05%

- Quarter-end effective duration for DBLTX was 4.05 and 6.71 for the U.S. AGG

- The top two performers were non-Agency residential MBS and non-Agency CMBS

- Agency MBS only slightly contributed to overall returns

Outlook

- We continue to hold this fund due to the approach and strong diversification factor within our core bond holdings

- DBLTX is a good position to hold due to its low duration which outperforms during periods of rising rates – Treasury yields were at all-time lows in 2020, but have flip-flopped in 2021

- Historically, DBLTX has displayed stronger returns and lower volatility than the index

- DBLTX has had consistent strategy, allocation focus, and sector distribution

[Category Mutual Fund Commentary]

Micah Weinstein

Research Analyst

Direct: 617.226.0032

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109