LISIX Commentary – Q2 2020

Thesis

LISIX is a bottom-up, growth-based fund that completes the core satellite strategy within global equity. The fund is unique in that it focuses on individual stocks rather than markets and looks for reasonably priced companies with strong growth potential. We like LISIX because of the managers’ expertise in various market caps, geographies, and sectors which helps keep the fund diversified while providing strong upside and downside capture over time.

[more]

Overview

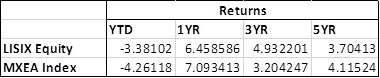

In the second quarter of 2020, LISIX outperformed the benchmark (MSCI EFEA Index) by 116bps. Quality factor tilt and stock selection in Financials and Utilities sectors contributed most to performance. While cheaper stocks continued to underperform, the fund sought out companies with strong financial productivity and inexpensive valuations. As valuation spreads between value and growth widen, the fund took advantage of cheaper stocks that helped provide balance to the portfolio, resulting in an overall relatively cheaper portfolio.

Q2 2020 Summary

– LISIX returned 16.04%, while the MSCI EAFE Index returned 14.88%

– Contributors

o Strong stock selection and underweight to Japan

o Volkswagen – German car company

o SAP – German enterprise application software firm

o ABB – industrial conglomerate situated in Switzerland

– Detractors

o Kao – manufacturer of consumer staples products in Japan

o Medtronic – medical devices located in Ireland

o Compass Group – high-quality catering and support services company in the UK

o Cash – largest detractor

Outlook

– We continue to hold this fund and believe in our thesis due to the fund’s strong stock selection, ability to find well valued companies, and expertise in various market caps, geographies, and sectors

– Historically, value has begun to outperform when their valuation is this cheap compared growth stocks and the global economy begins to accelerate

o With economies continuing to reopen and government policy helping provide liquidity and demand, a long recovery could end up supporting value stocks

– Looking for buying opportunities going forward in relatively inelastic industries, strong franchises, and cyclicals

[Category Mutual Fund Commentary]

Micah Weinstein

Research Analyst

Direct: 617.226.0032

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109