Applied Finance Select Fund Commentary – Q1 2021

Thesis

AFVZX is our only active manager in the large cap U.S. equity markets and applies a quality and value tilt to their investment strategy, holding roughly 50 companies. By utilizing DCF models, bottom-up fundamentals, and holding sector weights that are equivalent to their benchmark (S&P 500 Index), the fund generates alpha over time purely through stock selection. We continue to hold AFVZX because of the team’s ability to compare stocks across all sectors which enables them to generate strong returns over the long run.

[more]

Overview

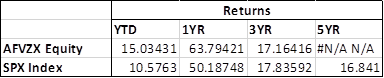

In the first quarter of 2021, AFVZX outperformed the benchmark (S&P 500 Index) by 602bps largely due to strong stock selection across 7 of the 11 sectors. Top contributors included Consumer Discretionary, Consumer Staples, Technology, and REITs. The fund’s consistent focus on “small and value” contributed to returns, while “large and growth” was out of favor. Communication Services and Healthcare underperformed by a 100bps.

Q1 2021 Summary

- AFVZX returned 12.19%, while the S&P 500 Index returned 6.17%

- No changes to the fund during the quarter – ALXN has agreed to acquire AZN in December 2021 and management plans to replace this name prior to the acquisition in Q3 2021

- Top contributors

- Consumer Discretionary – DRI and LKQ

- Consumer Staples – WBA and TSN

- Information Technology – HPQ, INTC, and KLAC

- REIT – HST

- Top detractors

- Communication Services – VZ and DIS

- Healthcare – PFE and MRK

Optimistic Outlook

- We continue to hold this fund and believe in our thesis due to the fund’s ability to outperform the index over the long run through strong stock selection and maintaining a quality and value investment tilt

- Value is seeing a strong rebound relatively to growth after is became “statistically” undervalued compared to growth

- Vaccine rollouts and the $6T deficit financed spending will turbocharge economy in coming years, but may result in high inflation, asset bubbles, and possibly fiscal crisis

- Increases in corporate and personal taxes may also create some hurdles due to an increase in difficulty of opening up a business and investors’ perception of a need for a higher rate of return

- Believe the fund’s holdings will continue to navigate the market well and positioned to perform strongly as the economy continues to reopen

[Category Mutual Fund Commentary]

Micah Weinstein

Research Analyst

Direct: 617.226.0032

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109