Current price: $218 Target price: $278

Position size: 3.8% TTM Performance: 4%

Key takeaways:

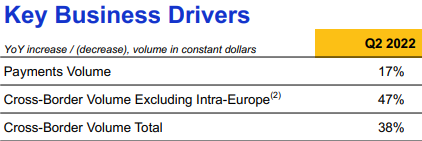

- Net revenue $7.2B +25% YoY vs street $6.86B. EPS $1.79 vs street $1.67.

- Cross border is key to growth and momentum keeps building – that strength drove their impressive beat. Cross-border was 25% of pre-pandemic revenues, it’s very profitable for them and still hasn’t fully recovered to baseline 2019….it’s ~90% of 2019 and, at historical run rates, would be 20-30% higher than 2019 levels. This suggests a continued steep recovery ahead which will be a strong tailwind to their business. Travel is a key driver and, more specifically, two of the biggest areas to recover are inbound int’l travel to the US and travel across Asia. The vast majority of the travel Visa captures on their credentials is consumer, and they are the global leader in travel co-branded cards.

- Inflation beneficiary – their fees are a % of transaction costs which rise w/ inflation

- Disruption fears overblown – they enable the disruptors, helping them rapidly scale and offer a strong value proposition for their fees, which are a small part of interchange. See more on this below.

- Reasonable Valuation… Visa is a high moat, duopoly company with extremely high FCF margins (over 50%), strong balance sheet and continued runway for secular growth driven by the shift from cash to card/digital payments and new payment flow opportunities (outlined below). Trading at ~3.5% FCF yield and compounding FCF/share at a high-teens %.

Quotes from the call…

- “In terms of the big picture, after a short four to five week impact of Omicron in December and January in the United States and many other parts of the world, the recovery continues to be robust. At this stage in terms of volumes, we have seen no noticeable impact due to inflation, supply chain issues or the war in Ukraine.”

- “Indexed to 2019, cross border travel, excluding transactions within Europe, jumped from a low of 71 in January to 94 in March”…”There’s plenty of recovery to come in one important corridor, inbound to the US, which indexed only at 70 in Q2″…and “Asia Indexed in the high 30s, both inbound and outbound in Q2.”

They expect accelerated revenue growth versus pre-COVID over the coming years, driven by 3 strategic levers:

- Consumer payments – enormous opportunity to displace cash and check globally ($18T) – the pandemic has helped accelerate this. Also a LT opportunity to grow the pie for digital payments w/ the 1.7 billion unbanked. This is driven by growing merchants, grow cardholders and new modes of acceptance. Many current trends in payments, including A2A, RTP, buy now pay later, crypto and wallet are enabling new ways to pay. Mgmt. says these represent opportunities for Visa (“We enable the disruptors”). Key to this is the easy onramp to their network, the instant scalability it provides to these new entrants, the value proposition w/ value identity protection, fraud prevention, dispute resolution, security, loyalty. Visa is agnostic to who wins this. They aim to sit in the middle as a “network of networks” and to continue to offer a high value proposition for the ~15bps that gets charged to merchants.

- Wallets: increasingly embed Visa credentials in their wallets to aid their own growth, so the consumer can use it anywhere Visa is accepted as well as receive and send cross-border P2P payments Wallet providers have been rapidly issuing Visa credentials that they see value in an open-loop ecosystem. Examples include Naranja X in Argentinian, PayPay wallet in Japan, Safaricom, the operator of M-PESA in Africa.

- Crypto: “leaning into in a very, very big way, and I think we are extremely well positioned”. Enabling purchases, enabling conversion of a digital currency to a fiat on a Visa credential, helping financial institutions and FinTech’s have a crypto option for their customers and upgraded their infrastructure to support digital currency settlement. They have over 65 crypto platform partners that are working with them. Also working with Central Banks as digital currency is being explored in many nations.

- E-commerce: closed a U.S. co-brand deal with Shopify. The Shopify Balance card will allow Shopify’s U.S. merchants to access funds from sales by the next business day and receive cash back on everyday business expenses like shipping and marketing.

- Buy Now Pay Later (“BNPL”): growth is coming in several ways. BNPL FinTech’s are issuing Visa credentials so they can scale through Visa’s broad acceptance. Affirm has chosen Visa as their network partner for the Affirm debit plus card. BNPL FinTech’s are increasingly using Visa virtual cards to settle with merchants. BNPL fintech consumers also continue to use their cards to pay off their instalments. And finally, for traditional issuers, they have a network installment solution called “Visa Installments,” which enables their financial institution clients to seamlessly offer BNPL capabilities through an existing credit credential on any Visa transaction.

- New Flows – 10X the opportunity of Consumer payments. With a $185 trillion in B2B, P2P, B2C and G2C. P2P, which represents $20 trillion of the opp., was Visa Direct’s first use case and continues to grow substantially. A key area of future growth is cross-border P2P, or remittance.

- Value-added services – includes consulting, technology platforms (e.g. Cybersource, issuer processing, and risk identity and authentication), data and insights, and card benefits, all which will improve with the recovery. Opportunity to increase penetration w/ existing clients. In 2021, 40% of their clients used five or more value-added services and nearly 30% use 10 or more. They expect sustainable high teens growth in this segment.

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

$V.US

[category earnings]

[tag V]