Share Price: $149 Target Price: $170

Position Size: 2.3% 1 Yr. Return: +22%

Key takeaways:

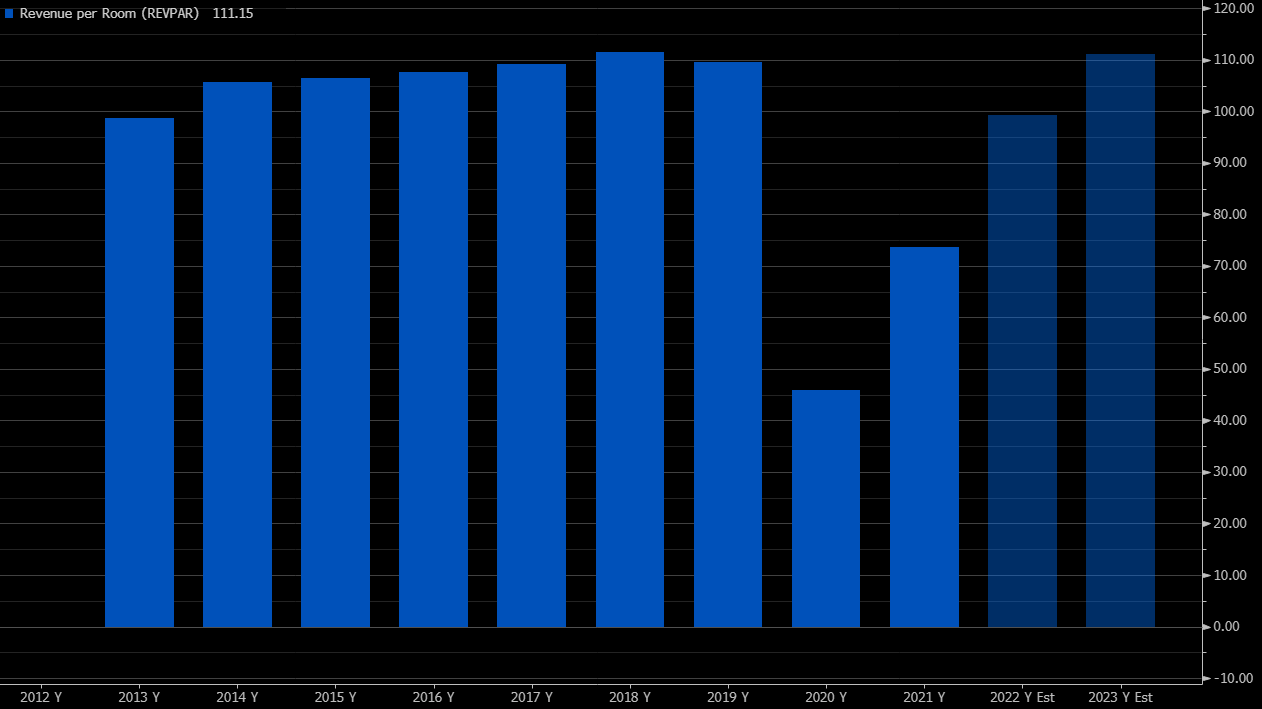

- Very positive quarter and strong progress on recovery – system-wide RevPAR increased more than 80% YoY, driving adjusted EBITDA up 126%. RevPAR was approximately 83% of 2019 levels with adjusted EBITDA at 90%. Beginning of the Q was impacted by omnicrom but improved. US leisure travel continues to be a key demand driver and is expected to stay strong. Recovery of group, business transient and Chinese (still down 47% vs 2019) and European markets will all be added tailwinds going forward.

- Leisure travel has more than recovered – leisure demand is well ahead of 2019 baseline.

- Business travel is recovering – US business transient RevPAR increased, sequentially, versus the fourth quarter, with March down only 9% compared to 2019 levels.

- “Inflation is our friend” – They have pricing power, re-price their product daily and have a significant portion of their revenues that are royalties tied to top line. Franchising is almost 2/3 of EBITDA and tied to top line, managing is another 25% of EBITDA where the fee stream is primarily base management fees (% of room revenue), with a smaller portion comprised of incentive management fees (% of hotel profitability). So, in an inflationary environment, pricing power = higher revenue growth and margin expansion.

- Stable room growth ahead, underpins LT growth story – They expect 5% room growth this year, accelerating to 6-7% longer term. The pipeline (~400K rooms) represents ~38% room growth from their current installed base of >1 million rooms and more than half are under construction (helps underpin several yrs. of predictable growth). Seeing very strong signings – rising rates not derailing development as demand for travel is increasing, hotels are the shortest duration leases in real estate and can increase prices w/ inflation, and in a tighter financing environment it helps to be associated w/ a banner, particularly one that commands the highest RevPAR premiums (which Hilton does). Almost 2/3 of their pipeline is located outside the US (franchise and mid-tier focus, tied to growing global middle class) – China is an important part of their pipeline and growth there is intact. Headwinds to construction from supply related issues (impacting unit growth this year) will abate.

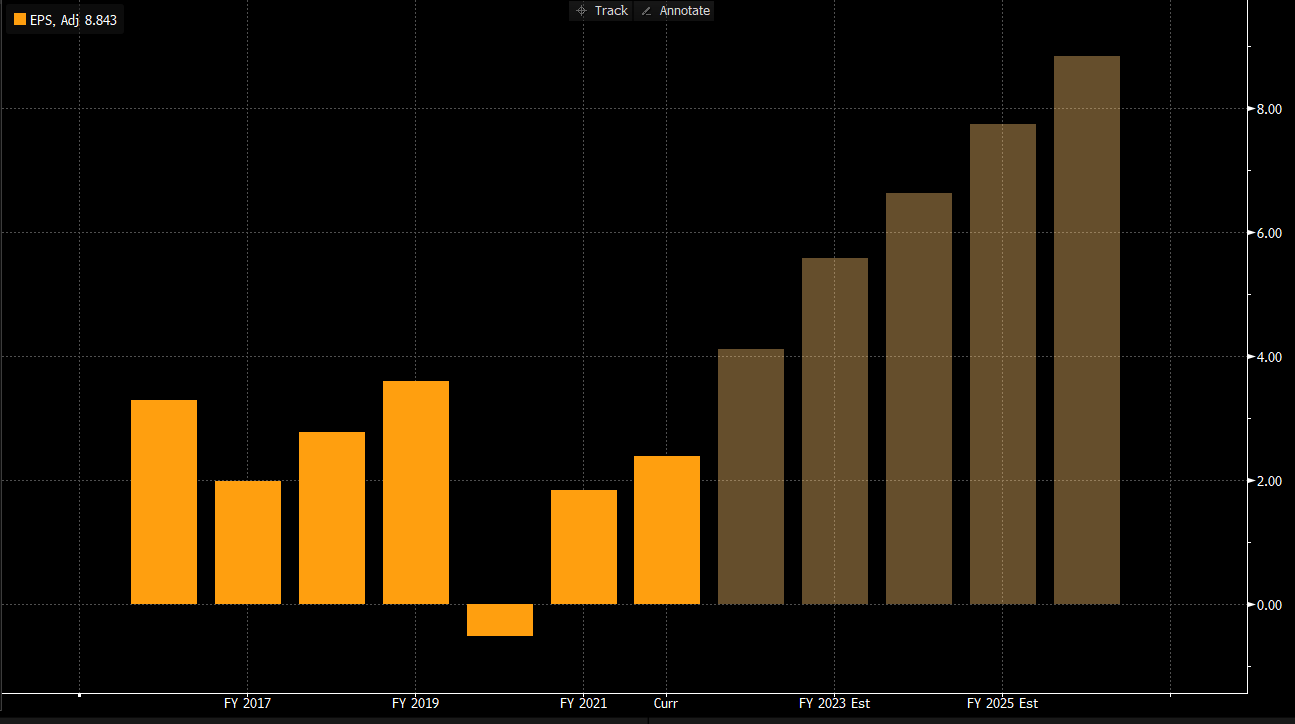

- Thesis playing out…profits recovering ahead of RevPAR as margins are going up…EPS this year is expected to be >14% above 2019 while RevPAR Tis expected to be 10% below. They expect permanent margin improvement versus prior peak levels in the range of 400 to 600 basis points over the next few years aided by cost efficiencies gained through Covid, including lowering labor intensity.

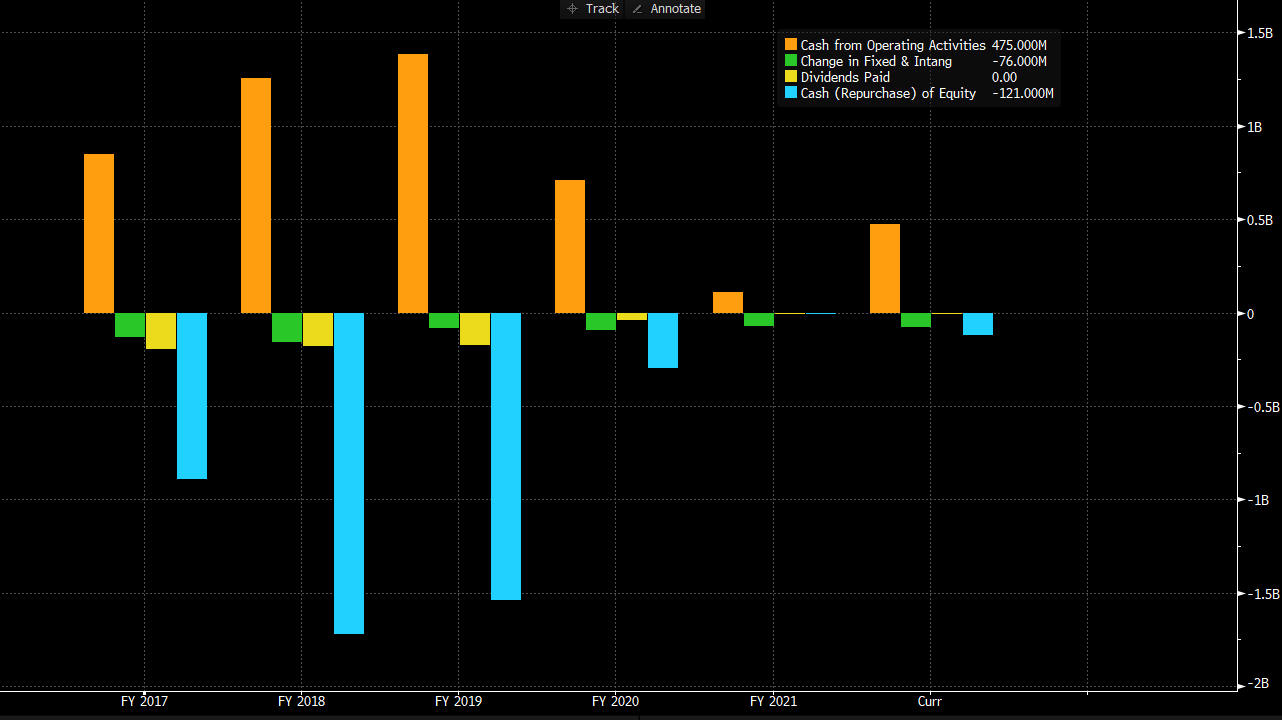

- Reinstated buybacks a quarter earlier than expected – targeting $1.4B-$1.8B for the full year in dividends and buybacks. Their fee-based capital-light business model and their industry leading RevPAR premiums coupled with further demand recovery, should continue to drive strong performance and meaningful FCF, which will enable them to return significant capital to shareholders. In the 3 years pre-pandemic, they reduced share count by ~15%…as RevPAR and FCF recovers, this level of buybacks should return.

- Valuation – PT of $170 based on very conservative assumptions of significant revenue growth this year and next as RevPAR recovers, then top line growth reverting to the low end of pipeline growth (6%) over the next few years (which imbeds no RevPAR growth) and margins below guided expansion. I included a 5 yr. historical P/E ratio chart at the bottom of the page. While it shows Hilton trading at an average P/E ratio…it’s not a very helpful way to think about their valuation as earnings collapsed in 2020, then the stock quickly recovered when a vaccine was announced (well ahead of earnings recovering)…moreover the current multiple imbeds enormous growth this year and next as RevPAR recovers.

RevPAR (Revenue per available room) expected to be 10% below 2019 baseline this year…while EPS is expected to be 14% higher than 2019…

In the 3 years pre-pandemic, they reduced share count by ~15%…as RevPAR and FCF recovers, this level of buybacks should return…

$HLT.US

[category earnings]

[tag HLT]

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109