Western Asset Core Bond Fund Commentary – Q2 2021

Thesis

WATFX (currently yielding 1.55%) is an actively managed fund that finds overlooked areas of the market that can go against consensus views and add value. Through internal macro, credit, and fundamental research WATFX identifies undervalued securities and takes on more credit exposure to generate alpha over time. Through a diversified approach to interest rate duration, yield curve, sector allocation, and security selection, the fund dampens exposure to volatility.

[more]

Overview

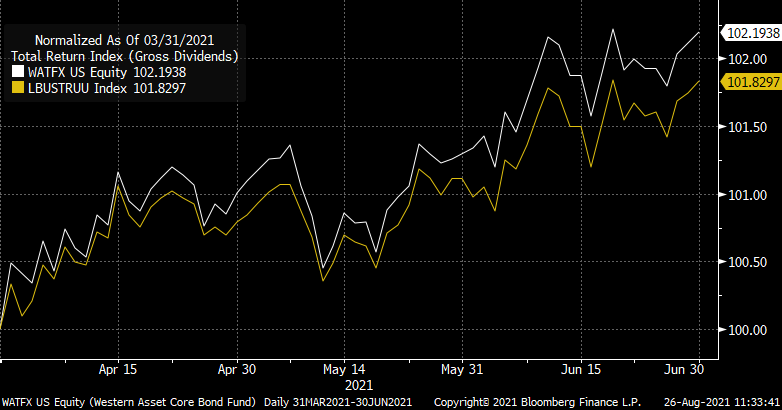

In the second quarter of 2021, WATFX outperformed the benchmark (Barclays U.S. AGG) by 36bps largely due to the fund’s duration and yield-curve positioning, as well as its investment-grade credit exposure. Spreads tightened in corporate credit and structured products which contributed to overall performance. In general, risk assets performed well for the quarter as inflation data came in surprisingly strong and the FOMC meeting in June resulted in rate hikes being pulled forward.

Q2 2021 Summary

- WATFX returned 2.19%, while the U.S. AGG returned 1.83%

- Quarter-end effective duration for WATFX was 7.10 and 6.58 for the U.S. AGG

- Trimmed duration, agency MBS, and investment-grade and “plain-vanilla” high yield debt

- Increased allocation to EM debt (US dollar-denominated corporate and sovereign bonds), reopening high-yield sectors, residential and commercial structured products, and banks loans

Outlook

- We continue to hold this fund and believe in our thesis due to the fund’s diverse approach and strong top down-bottom up fundamental value investing over the long-term

- Expecting global GDP growth to be strong, with higher inflation as the world economy continues to open

- Spread products should benefit most from reopening

- The fund is excited to seek out opportunities as spreads widen and the Fed continues to support corporate credit markets

[Category Mutual Fund Commentary]

Micah Weinstein

Research Analyst

Direct: 617.226.0032

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109