McCormick (MKC) delivered 1Q 2018 adjusted EPS of $1.00, a 32% increase y/y thanks to recent acquisitions and good product portfolio management. We are encouraged to see good progress on the margin front with continued stable top line growth. Management provided additional details on its cash use following the tax reform. Price target unchanged.

Research Blog – INTERNAL USE ONLY

The Blockchain Pipe Dream

A different view of blockchain from Nouriel Roubini and Preston Byrne

https://www.project-syndicate.org/commentary/blockchain-technology-limited-applications-by-nouriel-roubini-and-preston-byrne-2018-03

Trump’s Tariffs

On March 1st, 2018 President Trump announced his intention to impose significant tariffs on steel and aluminum imports. The announcement sent stock and bond prices falling, stoking fears of higher prices and slower economic growth. Protecting domestic industries like steel and aluminum may have raw appeal, but tariffs are flawed in theory and have a history of hurting economic growth. History shows a link between tariffs and populism which last flourished in the 1930’s. President Trump’s proposed tariffs threaten the post WWII global trade order and stock and bond markets are now paying attention.

Tariffs are bad policy

Basic economics instructs that tariffs benefit a select few producers and harm consumers through higher prices as they reduce competition and allow less efficient producers to continue to operate. In 1776, Adam Smith wrote of comparative advantage stating that countries should focus on their low cost production and trade for goods where their costs of production are relatively high. In general, society benefits from trade as wealth rises everywhere.

Tariffs have a consistent history of reducing economic activity and hurting growth1. The clearest example is the infamous Smoot Hawley Tariff Act of 1930, which essentially doubled tariffs on over 20,000 imported goods to an average rate over 50%. While this was one of many policy errors that contributed to the depth and length of the Great Depression, there is general agreement that these tariffs made matters worse. The effect of these tariffs on global trade are clear – from 1929 to 1933 world exports collapsed by roughly 55%.

Interestingly, there are many similarities between the 1930’s and today. Populist politicians flourished during both periods due to voter anger at 1) wealth and opportunity gaps, 2) perceived cultural threats, 3) established elites, and 4) claims of the government not working2. Both periods have similar economic overtones – low interest rates, low economic growth, stagnant wage increases and high debt burdens. In 1930, over 1,000 economists sent President Hoover a petition expressing their opposition to the Smoot Hawley bill, asking for his veto. President Hoover disregarded the petition due to voter anger at established elites. In a similar fashion, President Trump has ignored the advice of many of his advisors with these tariffs.

Politically, tariffs are easy to implement and hard to remove. One example is the Chicken Tax levied by France and Germany in the early 1960’s3. Success of U.S. chicken exports to Europe caused outcries from European farmers who lobbied politicians to tax chicken imports at 25%. The U.S. retaliated by taxing pickup trucks and commercial vans at 25%. Both sides of this tax remain in place today. In the market for sedans, foreign competition has improved car quality and choice for consumers, with even U.S. auto producers compelled to build better cars to compete. Consumers benefit from imports through improved quality and lowered prices for sedans, while competition and improvements for trucks and vans has lagged.

Anticipated effects of taxing steel and aluminum imports

Higher prices. For certain we can expect these tariffs to result in higher prices. Steel and aluminum are key inputs for production for companies in the U.S. Higher raw material prices will put U.S. producers at a competitive disadvantage against foreign producers. In recent stock market action U.S. car and plane manufacturers have been hit hard.

Job losses, not gains. The U.S. last imposed steel tariffs under President Bush in 2002. The project was abandoned after 20 months when a 2003 report estimated that the tariffs cost in excess of 200,000 jobs—more than the total number of people then employed in the entire steel industry at the time4. Today, steel makers employ about 140,000 workers while industries that use steel as an input employ some 6.5 million Americans. Transportation industries like aircraft and autos account for about 40% of domestic steel consumption and will have to pay higher prices for steel. These tariffs will hurt U.S. competitiveness globally5.

As with the coal industry, automation, not falling production, has been a big part of the secular decline in workers employed. The Wall Street Journal recently highlighted a Voestalpine AG steel plant in Austria that employs 14 people today to produce 500,000 tons of steel a year. That output would have required 1,000 employees in 1960.

Retaliation. Expect the EU and other countries not exempted from the tariff to implement their own tariffs on U.S. goods. Likely candidates include agriculture, cars, motorcycles, airplanes and even Jack Daniels. Foreign politicians will try to hurt the U.S. in very specific ways to invoke the strongest political response. Think chickens = pick-up trucks.

Missed target? By far our largest trade deficit is with China which totaled $375.2 billion last year. President Trump’s steel and aluminum tariffs will not affect China’s trade surplus with the U.S. Canada is hit hardest by these tariffs as they are the largest exporter to the U.S. for both aluminum (56% of U.S. imports) and steel (16% of U.S. imports).

Security threat? President Trump justified the tariffs by claiming our national security was at risk. This broad rationale applies to all countries who export steel and aluminum to the U.S. Prior administrations used tariffs for anti-dumping protection to single out one country who was selling in the U.S. at a price below their cost of production. The ‘national security’ clause is a rarely used nuclear option which sidesteps World Trade Organization rules. The claim is a bit thin as the U.S. imports only 30% of total steel used and all steel used by armed services is produced domestically. By claiming this option the U.S., as the world’s largest economy, has opened the door for other countries to follow. If countries side step existing trading laws and norms, the post-world war II trading order will be in jeopardy.

Markets reacting to political risks

The tariff announcement seemed rushed as evidenced by the disagreement within President Trump’s administration and key committee heads in Congress who were unaware of the details. Speaker Paul Ryan has urged President Trump to reconsider and provide exemptions for certain countries. Until this tariff announcement, President Trump’s actions have been mostly pro-business and pro-growth which has allowed the market to shrug off many of his volatile statements and provocative tweets. Perhaps markets start to pay more attention to his tweets and comments.

Unfair trade?

President Trump evaluates trade relations based on size of current account deficit. Trade deficits do not necessarily make a country poorer as it ignores the effects of the offsetting capital account6. Dollars used to buy foreign goods (less the value of our exports) flow back into the U.S. as investment. Since the U.S. trade deficit of the past 10 years has averaged $560 billion per year, there has been a lot of foreign capital flowing into the U.S. Foreign governments own a whopping $6.3 trillion of U.S. Government debt which is 33% of the total government debt. The U.S. benefits through lower interest rates. However, capital flowing into U.S. can be excessive, increase asset prices and in some cases cause asset bubbles. Foreign capital definitely helped fuel the housing bubble from 2004 to 20077. In theory trade deficits will weaken a country’s currency and the trade imbalance will self-adjust, because imports get more expensive and exports get cheaper as the dollar falls. Instead surplus countries have used their dollars from trade to buy U.S. assets averting currency markets, which explains why the U.S. has run a large persistent deficit since 1991. While President Trump’s view of deficits is overly simplistic, there is room to improve trade relations. Instead of harmful tariffs, finding a way to balance capital accounts would lead to more free currency markets and balanced trade.

There are other ways trade can be ‘unfair’. Foreign government subsidies, unconstrained ability to pollute, and cruel labor practices can give foreign companies a big cost advantage over U.S. companies. Socially conscious firms like Whole Foods promote ‘fair trade’ goods for their like-minded consumers. Mandating a level playing field for benefits and working conditions globally would help U.S. workers and improve U.S. relative competitiveness. Admittedly, these changes would be difficult to implement, but Trump’s anti-trade message has resonated with many voters.

Portfolio

During periods of uncertainty, portfolio diversification is paramount. We continue to be well positioned in high quality and short duration fixed income investments. We expect the trend towards higher inflation will benefit our alternative investments. Higher energy prices are a tailwind for MLPs and real estate managers tend to be good at raising rents to keep pace with inflation. For individual stocks, we continue to focus on companies with strong return on invested capital. While we cannot predict new tariffs, we believe our quality portfolio will weather the ups and downs of the market.

On March 2nd, President Trump tweeted “Trade wars are good and easy to win”. We believe neither to be true.

- https://www.cato.org/publications/commentary/truth-about-trade-history

- https://www.bridgewater.com/resources/bwam032217.pdf

- https://www.npr.org/sections/money/2017/01/25/511663527/episode-632-the-chicken-tax

- https://www.theatlantic.com/politics/archive/2018/03/steel-tariffs-consequences/554690

- https://www.wsj.com/articles/trumps-tariff-folly-1519950205?mod=searchresults&page=1&pos=2

- http://carnegieendowment.org/chinafinancialmarkets/67867

- https://ftalphaville.ft.com/2017/10/02/2194387/guest-post-the-real-cause-of-the-americas-housing-bubble-was-foreign-money/

Market Volatility and Sticking to Strategic Allocation

We constantly see different ways to depict the narrative, but I found this interesting. The author uses equity flows as the proxy for investor movements, indicating a “following of the crowd” type scenario.

The simple conclusion drawn from this illustration is that a balanced portfolio that remains balanced over time tends to outperform. The more investors move in and out of cash or “less risky” assets in an attempt to time market movements, the more likely they are to miss out on the upside or lose on the downside.

Continue reading “Market Volatility and Sticking to Strategic Allocation”

MLPs – FERC Ruling

Last week, the Federal Energy Regulatory Commission changed a ruling that will affect the revenue and cash flow for a few MLPs. Below discusses the policy change and what it means for the industry going forward.

The general consensus is that there will be a limited number of companies directly affected by the change, and the market selloff in the space was an overreaction. Nearly all management companies have provided commentary to this point, with the majority downplaying the negative effects of the ruling.

1.) What was the policy change that took place?

On March 15th, the Federal Energy Regulatory Commission (FERC) ruled that FERC regulated MLP owned pipelines can no longer recover the cost of income taxes in setting tariffs on interstate pipelines. Even though MLPs do not pay taxes, they were able to add in the tax rate of shareholders. Airlines fought this rule and won a change to the tax law. Therefore, the rate that MLP owners of FERC regulated natural gas and oil pipelines can charge customers must be lower to solve for the same ROE, reducing some MLPs’ cash flow and dividends.

There are four different price rate methodologies used currently. Only companies using the cost of service method will be affected. The cost of service is the revenue a regulated pipeline must collect from customers to cover its costs to operate. Following the announcement, income taxes will no longer be part of the total cost equation, implying that total cost of service will be lower, thus reducing cash flows from an asset.

2.) Which assets are impacted?

The only pipelines that will be affected are those which are currently regulated by the FERC and cross state borders. Additionally, these assets must use the cost-of-service method for pricing in order for the ruling to have a negative impact.

Management companies have come out and downplayed the effects of the change, noting that only a small portion of assets would be impacted. Based on a few different estimates, a worst case scenario would lead to an approximately 4.5% reduction of income due to decreased pipeline tariffs. Below is a flow chart showing the assets that will be negatively affected.

3.) How will TORIX be affected and what are their thoughts moving forward?

Looking at their holdings, Tortoise estimates the EBITDA reduction will be 2% or less. These numbers are based on current EBITDA and do not account for any new projects. Because new projects have tended to use market-based rates, they would generally not be affected by the ruling.

Tortoise MLP and Pipeline fund holds 25% (or less) of MLPs and owns 75% (or more) of C-Corp companies, so they have lower exposure to MLPs than the Alerian Index which is 100% MLPs. If a pipeline is publicly owned, it can be structured as a MLP (Master Limited Partnership) or a regular corporation (C-Corp). MLPs have a tax advantage when raising capital as the MLP does not pay taxes and can yield more.

This FERC tax rule change and Trump’s Tax Cuts and Jobs Act of 2018 have reduced the tax efficiency of MLPs relative to C-Corp firms, but have not eliminated the advantage. Depending on a MLP’s assets and finances, it may make sense for some of them to convert into C-Corps. Tortoise can own MLPs or C-Corps and can take advantage of any mispricing around potential changes in corporate structure.

With the selloff in the MLP space last week, we believe that Midstream energy company valuation are very compelling and continue to offer attractive yields. The yield of the Alerian MLP index is now at approximately 8.5%, which is compelling given REIT and utility yields are below 4%. While TORIX yield (3.16%) is lower than AMJ’s, the fund has outperformed the index by over 30% during the past two calendar years, showing the benefits of owning C-Corp midstream firms.

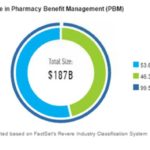

Currently, these tax law changes have placed a cloud over MLPs and the midstream energy space for investors. Despite this fog, fundamentals remain strong as the price of oil is above $60, gas and oil volumes continue to grow and MLP enterprise value to EBITDA valuation is attractive (see below charts). While we are disappointed in year-to-date performance, we are being patient and waiting for investor sentiment to improve.

US production of crude oil and natural gas has been strong:

MLP valuations remain low – close to 2 standard deviations below the mean:

Peter Malone, CFA

Research Analyst

Direct: 617.226.0030

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109

PLEASE NOTE!

We moved! Please note our new location above!

JP Morgan Guide to Retirement 2018

From: Peter Malone

Sent: Tuesday, March 20, 2018 9:46 AM

To: CrestwoodAdvisors <crestwoodadvisors@crestwoodadvisors.com>

Subject: JP Morgan Guide to Retirement 2018

Good Morning,

Attached is the 2018 JP Morgan Guide to Retirement. As always, JPM provides so much useful content, and this piece is extremely relevant to all areas within the Crestwood team.

I have included just four graphics that stuck out to me but would recommend looking through the full presentation whenever you have the chance.

Cigna to acquire Express Scripts

Cigna is acquiring ESRX for a 31% premium ($48.75 in cash and 0.2434 in stock). This deal validates the shift towards vertical integration in the healthcare space, as the different players try to resolve the continued pricing pressure and recent Amazon threat.

I believe standalone PBMs will disappear from the system, especially smaller PBMs that won’t be able to compete as well, although they only control 8% of the market currently.

According to the Insurance Information Institute, there are 858 health insurance companies in the US, which leaves room for the major players to keep gaining shares. Major mergers have been blocked by the Justice Department (Anthem/Cigna and Aetna/Humana), but by integrating PBMs with their insurance operations, majors insurance companies will squeeze out smaller players as they will be able to negotiate better terms for their clients.

My assumptions is that the integrated PBM business will over time no longer grow from outside health insurance contract wins, but support the growth of their own insurance business (with a better margin and revenue growth profile in the mid-single-digit range).

What sets CVS/Aetna apart is its retail pharmacy network and growth potential in the MinuteClinics. UNH is now trying to replicate this MinuteClinic model by acquiring small clinics/urgent care centers, and recently made a bid for Envision (an ambulatory outpatient surgery center such as ophthalmology – FYI I tested it in Boston a couple years ago, it wasn’t that bad and very convenient).

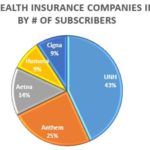

Health care Insurance companies market share (the left chart is a bit outdated, as it is from 2015):

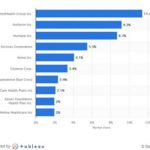

PBM Market shares (a bit outdated, as this is from 2016, and Express Scripts lost the Anthem business, representing 20% of their revenue):

Julie S. Praline

Director, Equity Analyst

Direct: 617.226.0025

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109

PLEASE NOTE!

We moved! Please note our new location above!

Fortive announces spin-off/split-off deal with Altra Industrial

This morning Fortive announced merging its Automation & Specialty business with Altra Industrial. The initial transaction details are below.

Terms of the deal:

Partly structured as a Reverse Morris Trust and as Direct Purchases of Assets & Equity interest:

· FTV will contribute a portion of FTV A&S businesses to the newly created subsidiary

· FTV will distribute the equity interests in Spinco to FTV shareholders in either split-off or spin-off

· Spinco will merge with a subsidiary of Altra, and as a result will become a subsidiary of Altra, and Spinco shareholders will receive 35M shares of Altra common stock

· Upon closing, FTV will own 54% of the combined company, and Altra 46%

Fortive A&S brands Kollmorgen, Thomson, Portscap and Jacobs to be divested to new Spinco ($907M in sales, $220M in EBITDA)

Fortive shareholders to receive ~$3B ($1.4B in cash proceeds and debt reduction, $1.6B in newly issued Altra common stock)

Transaction expected to close by the end of the year

Continue reading “Fortive announces spin-off/split-off deal with Altra Industrial”

SSGA – Uncommon Sense

Good Afternoon,

Attached is the most recent “Uncommon Sense” piece put together by Michael Arone at SSGA. The theme is the recent increase in volatility, and he discusses the following three points:

1.) Investors have relied on the “Fed Put” during the market run-up, and he believes this remains in play with the new Fed Chair, Powell

2.) We are still in a Goldilocks market environment, with modest “not too hot, not too cold” growth

3.) Fundamentals continue to be the driver of growth in the stock market, and the numbers continue to be solid

TJX Q4 Earnings Update

TJX reported a great Q4 amid a difficult retail environment. Sales were up 8% on 4% SSS and 4% square footage growth. Notably, traffic was the primary driver of SSS at all of their concepts. Comp store sales exclude e-commerce, which is still small but “grew significantly.” Total global store count now stands at 4,070. They clearly have the model in brick and mortar that is working. They opened 250 stores in 2017 as other retailers continue to shrink their store count. They plan to grow stores 6% this year with most of the growth coming from their home concepts. They increased their dividend by 25% to $1.56, putting them close to a 2% yield.

- Marmaxx, their largest division, had 3% SSS on positive traffic and negative ticket.

- Overall merchandise margins are strong though there was some contraction at HomeGoods.

- Same store inventories were up in-line with sales.

- Wage increases negatively impacted EPS growth by about 1%.

- 2018 FCF was $2B and they returned $2.4B to shareholders.

- They plan to repatriate $1B in cash in 2019

Current Price: $84 Position Size: 2%

Price Target: $84 TTM: 5.4%

Guidance:

- 2019 sales of $37.7B, +5%. Assumes SSS of 1-2% and 6% store growth.

- 2019 EPS: $4.04, +5%, assumes an increase in merchandise margins.

- Wage increases will negatively impact EPS by 2% and will continue to have a negative impact beyond 2019.

- Fx should be about a 1% benefit.

- For SSS by division they expect:

- Marmaxx +1-2%

- HomeGoods +2-3%

- Canada +2-3%

- International 1-2%

Inventory Availability:

- There have been investor concerns that inventory is getting more rationalized at retailers resulting in fewer closeouts and less available inventory in the off-price channel.

- Management addressed this on the call saying that, “availability has never been an issue for TJX in over our 41-year history. Throughout 2017 overall availability of inventory from top vendors was as good as it has ever been.”

- They are one of the most efficient and discrete channels for vendors to clear inventory, whereas clearing inventory online is not as discrete and can be brand damaging.

- Their sourcing scale is part of their competitive advantage and they source from 20k vendors in 100 countries.

- Additionally, on the call management pointed to online vendors as a new source of inventory.

Future growth will rely increasingly on the Home category and International:

- Given this, management is looking towards the home category as their next leg of growth. They are accelerating store openings and are bring the Canadian HomeSense concept to the US.

- One the call they introduced a long-term store target for HomeSense in the U.S. of 400 stores, from the 4 stores today.

- They also expect to add 483 HomeSense stores in Canada, bringing the total there to 600.

- In Europe, they are the only major off-price retailer.

Valuation:

- Their balance sheet is strong with no net debt.

- Store openings will bolster top line growth.

- They have been steadily FCF positive with LT FCF margins averaging about 6-7% and high ROIC.

- Assuming a normalized FCF margin, they trading at about a 5% forward yield.