Current Price: $139 Price Target: $150

Position size: 6.4% TTM Performance: 31%

Microsoft reported solid Q4 results with better than expected growth in all segments. Cloud continues to be the key driver. Q4 revenue was $31B (+14 YoY constant currency) and EPS was $1.37 (+24% constant currency). Commercial Cloud business was up 39% and saw continued margin improvement, helping to drive op income up 24% constant currency. Counted w/in that is Azure, which was up 73%. They are taking share from Amazon’s cloud offering, AWS. This should continue as they are better positioned as more large enterprises, that are longtime customers, move to the cloud. Just two days ago AT&T chose MSFT’s cloud – one of their largest cloud commitments to-date. Given their enterprise customer base, recent partnerships with VMware and Oracle, and superior Azure hybrid architecture, the company is uniquely positioned to capitalize on the growing demand for cloud services.

Key Takeaways:

· Solid growth across all 3 segments:

o Productivity & Business Processes, up 14% YoY, $11.1B

o Intelligent Cloud, up 19% YoY, $11.4B

o More Personal Computing, up 4% YoY, $11.3B.

· For the full year Commercial Cloud (consisting of O365 Commercial, Azure, Dynamics Online, and LinkedIn Commercial – this includes some revenue from the first two segments above) was $38B. That’s 30% of total revenue, and grew 39% in the quarter.

· Within Commercial Cloud, Azure growth was 64% YoY (68% constant currency) vs. 75% cc last quarter.

· Commercial Cloud gross margins improved 600bps YoY and 200bps sequentially, driven by material improvement in Azure gross margin.

· Similar to last quarter, the only area of weakness was gaming.

Valuation:

· For the full year they returned $30B to shareholders.

· Trading at a 3-4% FCF yield –still reasonable for a company with double digit top line growth, high ROIC and a high and improving FCF margins.

· They easily cover their 1.3% dividend, which they have been consistently growing.

· Strong balance sheet with about $134B in gross cash, and about $56B in net cash.

Investment Thesis:

· Industry Leader: Global monopoly in software that has a fast growing and underappreciated cloud business.

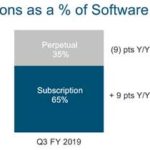

· Product cycle tailwinds: Windows 10 and transition to Cloud (subscription revenues).

· Huge improvements in operational efficiency in recent quarters providing a significant boost to margins which should continue to amplify bottom line growth.

· Return of Capital: High FCF generation and returning significant capital to shareholders via dividends and share repurchases.

$MSFT.US

[tag MSFT]

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109