Disney presentation from today’s meeting.

$DIS.US

[tag DIS]

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

Disney presentation from today’s meeting.

$DIS.US

[tag DIS]

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

Alphabet is down pre-market – they reported earnings, missing on the top line and beating on EPS. This is a quick summary – I will follow up with more details. Management attributed the revenue miss primarily to Fx and also the timing of some ad product changes. Revenue was $36.3B vs. consensus of $37.3B, up 19% constant currency (17% reported) – that’s a deceleration from 23% in 4Q18. Excluding the impact of the EU fine EPS was $10.81, better than consensus of $10.53.

$GOOGL.US

[tag GOOGL]

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

Current Price: $160 Price Target: Raising to $185 from $160

Position Size: 3.8% TTM Performance: 32%

Visa continued to perform well in the second quarter with better than expected revenue and EPS. Net revenues were up 9% (constant currency), dampened by higher client incentives. EPS was $1.31 vs consensus $1.24. They reaffirmed full-year 2019 net revenue growth of "low double-digits" on nominal basis and slightly increased adjusted EPS growth to "high-end of mid-teens," from "mid-teens.” Slight weakness in the quarter was that volume growth decelerated from 11% to 8%. Mgmt said volume growth was impacted by fewer processing days in the quarter and timing of Easter. Processed transactions continued to see double-digit growth. Last quarter they expressed concerns around weakening non-US macro trends and cross border transactions, but this quarter they struck a more positive tone, indicating that cross border had stabilized. Cross border accounts for ~27% of gross revenue and is higher yield. In the first few weeks of Q3, payment vols have accelerated, especially in the US.

We are recommending buying Disney to 2% and selling Sanofi to fund the purchase, remainder from IVV.

Disney Investment Thesis:

Rationale for selling Sanofi:

· Our portfolio is overweight in Healthcare which prompted our review of names we own in this sector:

· Top line growth is below other healthcare names we own

o Their biggest drug (Lantus) has seen big decline in sales in the past 5 years, as have other Pharma names, but other drugs developed by SNY have not offset the decline in $

o Although Genzyme has been a successful acquisition story, it took Sanofi 7 years to execute on another major acquisition (Bioverativ) that could bring back some top line growth (which hasn’t materialized yet)

· Their Vaccine segment saw some headwind from its Deng vaccine program in the Philippines, possibly resulting in 100 children deaths.

· While its dividend is attractive (4.2% yield), the stock has not delivered on expectations

$DIS.US

$SNY.US

[tag DIS]

[tag SNY]

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

Current Price: $459 Price Target: $540 (Increasing from $480)

Position Size: 2% TTM Performance: +14%

SHW reported a weak 1Q, missing estimates on lower volumes across all three segments. They saw a slow start to the architectural painting season in N. America and continued challenging conditions in “many end markets outside N. America.” Despite this, the stock is up on positive outlook in N.A. w/ an expected rebound in volumes in 2H and better gross margin performance. Despite miss, management reiterated full year EPS guidance (+13.5% YoY). Very positive commentary on expectations for N. America paint stores (drives majority of their profit) on an expected improvement in housing turnover. In addition, price increases and declining raw material pressure may lead to positive revisions on improved margin expectations.

Key Takeaways:

· SHW is set to benefit from higher product prices, good volume growth, falling raw material costs and an improvement in housing.

· Gross margins improved sequentially, flat YoY, despite the volume shortfall and higher raw material costs. This is encouraging given mgmt. expectation that YoY raw material inflation will be highest in Q1. They expend continued GM expansion and expect volumes to improve over the balance of the year, particularly in the back half.

· They saw broad based softness in Asia and Europe.

· The Americas Group: 55% of sales, +3.6%

o Despite a strong backlog and project pipeline reported by their professional customers, volume growth was slower than expected.

o Weakness this quarter is not a cause for concern. This is the seasonally smallest quarter for their paint stores business, and can be volatile year-to-year. Better indicator of demand is painting contractor’s feedback on project backlog. They are universally optimistic, report seasonably high project backlogs and a very healthy pipeline of new projects.

o They would be a big beneficiary of an improvement in the housing market.

o Opened 15 new stores

· Consumer Brands Group: 16% of sales, down less than 1%

o FX headwinds(-1.6%)

o Most of the softness in demand in the quarter was in markets outside North America, most notably Asia-Pacific.

o Operating margin in the first quarter expanded sequentially and YoY

o “we are very well positioned across all North American retail channels heading into the important spring selling season.”

· Performance Coatings Group: 29% of sales, modest sales growth

o Operating margin improvement despite raw material pressure.

· Guidance Reaffirmed

o Sales guidance for Q2 +2-5%; full year +4-7%

o Reaffirmed full year 2019 adjusted diluted net income per share guidance to be in the range of $20.40 to $21.40 vs $18.53 in 2018. Midpoint slightly below street.

Valuation:

Thesis:

$SHW.US

[tag SHW]

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

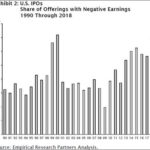

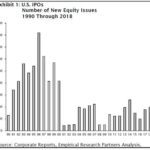

While the number of IPO’s hitting the market is not close to the levels of the dot-com era, the share of current IPO’s that are losing money is approaching levels last seen in the late 90’s.

Thought this was interesting given the series of high profile IPOs expected this year. Lyft recently went public (losing money and trading below offering). Other potential IPOs this year include: Uber, Airbnb, Slack, Palantir Technologies, Robinhood, Beyond Meat, Zoom, Pinterest, Postmates, WeWork.

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

· Yesterday the European Parliament passed the EU Copyright directive (see original email from Sept. below) which is primarily targeted at Google and Facebook.

· The directive includes 2 key articles – Article 11 (the ‘link tax’) and Article 13 (the ‘upload filter’). The Link Tax gives publishers the right to charge for linking to their content and the Upload Filter would put the obligation on platforms to identify what is copyrighted by making them liable for copyright infringement. Commercial deals with publishers would be required in order for Google to show hyperlinks and short snippets of news.

· Those in favor (content creators) say it protects their product, giving publishers a negotiating edge w/ Google and Facebook. Those against it say it limits the free access of the internet. Part of the concern is that the directive is vague and it’s difficult to precisely filter out what’s copyrighted and what’s not – the result may be over-blocking content in an effort to limit the risk of an infringement. The wording of the directive is apparently ambiguous enough that the impact it will have is not entirely clear and may become more clear in the future – countries may interpret the directive differently.

· User generated content on places like YouTube and Facebook would need to be filtered. Google already does this to an extent on YouTube.

· Google News would need to license all the content that shows up in search results. Google put out the screen shot below of what News search results would look like without licensing.

· Google says “we built Google to provide everyone with equal access to information”…”Article 11 means that search engines, news aggregators, apps, and platforms would have to put commercial licenses in place, and make decisions about which content to include on the basis of those licensing agreements and which to leave out.” As a result, Article 11 would mean Google is picking winners and losers based on who they establish commercial agreements with (likely the largest publishers).

· The revenue impact to Google should be limited. EMEA is about 1/3 of revenue. Ad revenue from relevant news sites in Europe is a small subset of that. Importantly, these same publishers make money by traffic landing on their sites via Google by selling ad space through Google’s AdSense product. The larger consequence may be more around limiting news results.

$GOOGL.US

[tag GOOGL]

From: Sarah Kanwal

Sent: Friday, September 14, 2018 12:33 PM

To: ”

Cc: CrestwoodAdvisors <crestwoodadvisors>

Subject: EU Copyright Directive

· The EU is on a path to create copyright laws aimed at helping publishers of content (e.g. journalists, musicians etc.) get a bigger piece of ad revenues that go to companies like Google and Facebook.

· The EU parliament voted in favor of the directive a couple days ago, but there are several more steps for this to pass.

· The new rules would give publishers the right to ask for paid licenses when a platform shares their stories (i.e. Google News) or video clips. Some are calling it a “link tax." The rules would also put the obligation on platforms to identify what is copyrighted by making them liable for copyright infringement.

· The implications aren’t entirely clear yet. For example, the rules would apply to “commercial platforms” but it’s not clear whether that applies to blogs etc., which would widen the impact.

· Other countries like Spain and Germany tried similar rules in the past and they failed. Google’s response was either to shut down Google News or just remove any news sources that wouldn’t give it free access…which meant traffic to those sites collapsed.

· The regulation might actually reinforce the dominance of the strongest players. The cost burden of this regulation would be easier for large firms like Google to absorb as it would require firms to build technology to identify and filter copyrighted content. Thus it might have the unintended consequence of strengthening Google (and other platform giants) relative to smaller firms/startups. In fact, Google already largely complies with these rules on YouTube with their “Content ID” filter.

· Opponents also say that complying with these rules would limit the free access of information that the internet is designed to offer.

· If this directive keeps progressing their will likely be more vocal industry resistance, as many who have been critical of the big tech firms don’t support it. For example, Tim Berners-Lee (inventor of the world wide web), who has spoken widely about the risks of Google’s and Facebook’s dominance, is ardently against these potential regulations.

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

Apple held an investor event today where they unveiled details about their new Service offerings:

· Apple News+ – $9.99/month news app w/ family sharing that includes WSJ, LA Times, 300+ magazines. Available today in US and Canada. Launching in Australia and UK later this year.

· Apple Card – new credit card in partnership with Goldman Sachs. No annual fees, no late fees and they said it would be a low interest rate. Also will include app that helps track purchases, pay balances and gives daily cash back ranging from 1% with physical card to 2% with Apple Pay and 3% on Apple purchases.

· Apple Arcade – subscription gaming service with exclusive content. Launches in over 100 countries in Fall 2019. Pricing not announced, but no ads and no in game purchases.

· Apple TV App – newly designed app for mobile and smart TVs that aggregates TV subscriptions from DirectTV, Amazon, Hulu, Showtime, HBO and more (Netflix did not sign on).

· Apple TV+ – New TV subscription offering with exclusive content. Launches in the Fall, pricing not announced yet. They had a long list of collaborators including Oprah, Steven Spielberg, Ron Howard, JJ Abrams, Steve Carell, Jennifer Aniston and lots more. Focused more on quality than on quantity. Spending a lot less on content than Netflix. Netflix spent about $12B last year. Amazon spent ~$4.5B and Apple is expected to spend closer to $2B… though that may go up.

Interestingly there was a lot of emphasis throughout the event that was clearly aimed at separating how Apple operates from how Facebook operates. The presentation on the news app was very focused on how the news would be high quality, curated content from reliable sources. And with each of the new products they emphasized privacy. They talked about how Apple would not collect data and often would not even have access to it. For instance with the TV app, the technology suggesting new TV shows based on viewing habits would sit on phones and not on Apple’s servers. With Apples News they won’t track what you read and they won’t allow advertisers to track you. They won’t track purchases with the Apple Card.

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

Current Price: $1,737 Price Target: $2,400

Position Size: 2.6% TTM Performance: -6%

Key Takeaways:

· Slight miss on revenue, beat on EPS. While revenue was below consensus, it was ahead of the high-end of their guidance.

· Weak guidance: disappointing Q1 guidance driven by a weakening European market (the vast majority of their revenue) and higher ad spend.

· They have a track record of conservative guidance – they almost always come in ahead of the high end of their bookings guidance on a constant currency basis.

· Europe softening – they witnessed a slow start to the year, primarily in their core European markets, which they believe is largely due to overall macroeconomic factors. Average daily rates were a little weaker than expected and they guided to a meaningful deceleration in room night growth.

· FX headwind is expected to be significant this year. Current rates assumed in guidance reduces gross booking growth, revenue growth and non-GAAP EPS growth by 250 bps for the full year and 500 bps for the first half.

· Investing for growth: this will compress Q1 margins by ~350bps and reduce their full year EBITDA growth by a few percentage points. This reflects increased spend on brand advertising, customer acquisition and incentive programs and spending to support their new payment platform. They are investing in a payment platform that supports non-hotel properties, and will facilitate growth in transport and local attractions business.

· 171 million worldwide room nights booked in Q4, up 13% YoY and ahead of the high-end of guidance.

· Gross bookings of $19.6B were a little lower than expected (+13% constant currency) a slight deceleration from +14% last quarter.

· Alternative accommodations: this is their business that competes with Airbnb and HomeAway. For the first time they disclosed revenue for this business – it now makes up 20% of revenue. They also said 40% of Booking’s active customers booked an alternative accommodation property at some point during the past 12 months.

· Growth vs. margins: They have been trying to “optimize” ad spend for several quarters by spending less on performance advertising (e.g. Google AdWords) and more on brand advertising (e.g. TV commercials). The idea is that brand advertising drives direct traffic to their site, resulting in a higher ROI. This ad spend/rev growth algorithm will continue to be a focus going forward as clearly the trade-off between growth and spend persist.

· Direct channel mix increased again (“well over 50%” of booked room nights). Probably not a coincidence that they now say over 50% of their bookings come from mobile devices, as mobile traffic is more likely to be direct (via app).

Current Price: $50 Price Target: $60 (updated for the stock split)

Position Size: 3.6% TTM Performance: 29%

TJX reported Q4 EPS that was in-line with the street and much better than expected SSS (+6% vs consensus +3.5% (guidance was 2-3%). Guidance was a little below expectations due to higher wage and freight costs and currency headwinds. For Q1 wage and freight will be a 7% drag on earnings, for the full year these are expected to be a 4% drag. It’s been a very mixed quarter of results for retailers so far. WMT, COST, TGT and now TJX have all stood out with strong results while others reported a poor holiday season, particularly department stores. TJX, along with other off-price retailers, captured market share in the US. TJX’s sales have doubled over the last 10 years despite a changing retail environment.

Key takeaways:

· TJS Q4 SSS were an impressive +6%. Traffic was again the biggest driver (SSS numbers do not include e-commerce).

· Performance was solid across all divisions and geographic regions.

· Core Marmaxx division (60% of revenue) delivered SSS growth of 7%.

· For the full year, HomeGoods was their fastest growing division with 10% square footage growth and 4% SSS.

· The margin pressure they are expecting from freight and wage increases is a continuation of trends they saw last year.

· Q4 gross margins were flat and inventories grew less than sales. For fiscal 2019 merchandise margin was essentially flat despite a significant increase in freight costs. Ex-freight, merchandise margins improved significantly.

· Optimistic comp guidance: Fiscal 2020 EPS outlook is based on SSS growth of 2%-3% (3%-4% at Marmaxx). This is notably positive because for at least the last 6 years, they have started the year with comp guidance of 1-2% and have ratcheted up that guidance as the year progresses.

· Announced they are launching e-commerce for Marshall’s later this year.

· Tariffs: when asked on the call about the impact of tariffs on product availability, mgmt. said longer term it’s probably going to be a benefit for them because any chaotic change in the way vendors manage or allocate product will ultimately benefit them.

· Continue to take share in Europe: In Europe comp sales grew 3% despite the challenging retail landscape. They have over 500 stores in Europe- in mainland Europe, they are in only 4 markets: Austria, Germany, Poland and the Netherlands. They also have stores in the UK