Good Morning,

Attached is the most recent chart pack put out by SSGA.

Thank You,

Pete

Peter Malone, CFA

Research Analyst

Direct: 617.226.0030

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109

Good Morning,

Attached is the most recent chart pack put out by SSGA.

Thank You,

Pete

Peter Malone, CFA

Research Analyst

Direct: 617.226.0030

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109

Pete and I created performance charts for our US large cap funds as a group compared to iShares 500 index ETF (IVV) and for Core US Bond funds as a group against the iShares Barclays US Aggregate Bond ETF (AGG). In our quarterly performance presentation we show performance of each vehicle and it was not clear that these funds as a group has performed well.

Here is a chart of performance of our US large cap funds against IVV going back to beginning of 2017:

A few observations from this chart:

1. Performance has been good especially considering only 22% of active managers beat the S&P 500 over the past 3 years.

2. Tracking error prior to the change in funds (9/28/18) was really low and was a main reason for the change

3. The funds as a group picked up 200 bips during the end of year downturn! The larger allocation to low vol has really helped.

I ran the same chart for our active bond managers against AGG – iShares Barclay US Aggregate ETF.

As you can see our collection of active bond managers has added value over iShares US Aggregate ETF.

Hopefully these charts help you explain the positive results to clients!

Thanks,

John

The senate hearing of the PBM industry included 5 major PBM players: CVS, Express Scripts (Cigna), OptumRx (UNH), Humana and Prime Therapeutics. Continue reading “Outcome from the PBM Senate Hearing yesterday”

Attached is the quarterly performance review presentation from the RM meeting on 4/9/19.

Thanks,

John

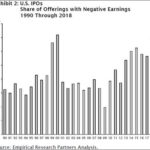

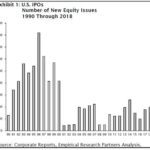

While the number of IPO’s hitting the market is not close to the levels of the dot-com era, the share of current IPO’s that are losing money is approaching levels last seen in the late 90’s.

Thought this was interesting given the series of high profile IPOs expected this year. Lyft recently went public (losing money and trading below offering). Other potential IPOs this year include: Uber, Airbnb, Slack, Palantir Technologies, Robinhood, Beyond Meat, Zoom, Pinterest, Postmates, WeWork.

Sarah Kanwal

Equity Analyst, Director

Direct: 617.226.0022

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square, Suite 500

Boston, MA 02109

We are trimming UNP 50bps and allocating the proceeds to IVV based on the following reasons: Continue reading “Trimming UNP”

Ray Dalio, head of Bridgewater Associates, published a great article on income inequality. The article links inequality to education and shows that the US lags developed countries in many categories. Dalio shows that high rates of workers earning less than than their parents and falling standards of living have lead to voter mistrust and disenfranchised populations, which has clearly been themes that Trump has tapped. He concludes that American capitalism is at risk.

Why-and-How-Capitalism-Needs-To-Be-Reformed

Thanks,

John

Key takeaways:

Current Price: $190 Price Target: $233

Position Size: 1.82% 1-Year Performance: +14% (since inception 12/20/2018)

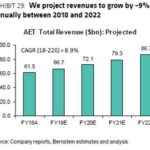

STZ reported its 4Q 2019 earnings results this morning. Beer shipment remains high at +8%, and total beer sales grew +9.3%. During the call, management highlighted the strength Corona and Modelo, in addition to their product innovation capabilities, as driving continued market share gains in North America. It was highlighted that 1Q20 will reflect some inventory destocking, so a slowdown in growth rate should be expected in 1Q20. Beer EBIT margin was above last year at 40.5% vs. 37.9%. Better price/mix and lower marketing spend helped expand margins.

In addition to today’s good results, last night they announced the sale of lower-tier wines (30 brands out of the 64 lower price owned by STZ) to E&J Gallo for $1.7B, allowing STZ to focus on premium, higher growth/higher margins brands. Those brands were $1.1b in sales in FY19 (38% of wine sales). This had been talked about by management but the deal is closing sooner than what we had anticipated. Overall we are pleased with the results and look forward to future announcement around the use of cash from the wine sale.

Continue reading “Constellation Brands (STZ) 4Q19 earnings summary”

Good Morning,

I have attached the updated Monthly Market Monitor from Eaton Vance.

Thank You,

Pete

Peter Malone, CFA

Research Analyst

Direct: 617.226.0030

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109

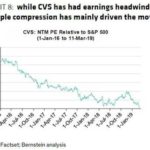

Why is the stock down?

There has been multiple events pushing the stock down:

· Omnicare underperformance that led to an additional write-down in 4Q18

· Loss of the Centene and WellCare business as those two clients merge and will bring the PBM in-house

Outside of their control:

· Democrat’s push for Medicare-for-all would impact health insurers (and recent Aetna acquisition)

· Removal of the rebates practice in the government side of the PBM business (CVS is #3 in this space)

· Drug Pricing Transparency Act: this bill would force PBM to pass all rebates to the point of sale and no longer be kept by PBM and/or health insurers

· Push to repeal Obamacare back in the news

· Walgreens had bad earnings and cut their 2019 forecast, pushing the sector down

Why remain invested in CVS?

1/ We find CVS’s long-term strategy of vertical integration compelling:

· This can truly help CVS differentiate themselves from competitors by offering a powerful value proposition, leveraging its network and developing predictive data analysis that will help them lower costs of care

· A similar strategy was successfully implemented by UNH who saw nice margins growth after the integration of Catamaran (PBM)

2/ Retail store footprint combined with MinuteClinic and their new HealthHub concept could become a great growth engine for CVS:

· The retail stores ($19.7B in sales, >10% of total sales) have suffered from lower foot traffic following the removal of tobacco sales

· Offering customers another reason to visit the stores/pharmacy thanks to their new Health & wellness concept (to become 20% of the square footage of the store) could revive traffic

3/ Valuation: we see a disconnect between today’s stock price and the value of its businesses:

· Our sum-of-the-parts and cash flow analysis both show an attractive risk/reward profile

We are currently reviewing our position size for this stock.

[tag CVS]

Julie S. Praline

Director, Equity Analyst

Direct: 617.226.0025

Fax: 617.523.8118

Crestwood Advisors

One Liberty Square

Suite 500

Boston, MA 02109